Closing Costs Explained: State-by-State Insights for Homebuyers

Buying a home this year? Don’t overlook closing costs.

Everyone knows they exist, but not everyone knows what’s inside or why the total can swing so much depending on location. Let’s break it all down so you’re not caught off guard at closing.

Breaking Down Closing Costs

When you buy a home, closing costs are the added expenses you’ll pay to finalize the deal. They apply to every buyer. Freddie Mac notes they often include homeowner’s insurance, title insurance, and a list of fees like:

- Loan application

- Credit report

- Loan origination

- Home appraisal

- Home inspection

- Property survey

- Attorney

National vs. Local: Why Closing Costs Vary

Most online sources will give you a national estimate for closing costs—typically 2% to 5% of the purchase price. That’s a helpful baseline when you’re building your budget, but it doesn’t capture the full picture. Your actual costs depend on:

- State and municipal taxes or fees (transfer taxes, recording charges)

- Local service costs (title, legal, and related professional fees)

While the price of the home is a major factor, what you’ll actually pay in closing costs also depends on state laws, local tax rates, and even typical charges for services like title and attorney work. That’s why it’s smart to connect with the experts early—so you know how to budget and feel confident before you begin house hunting.

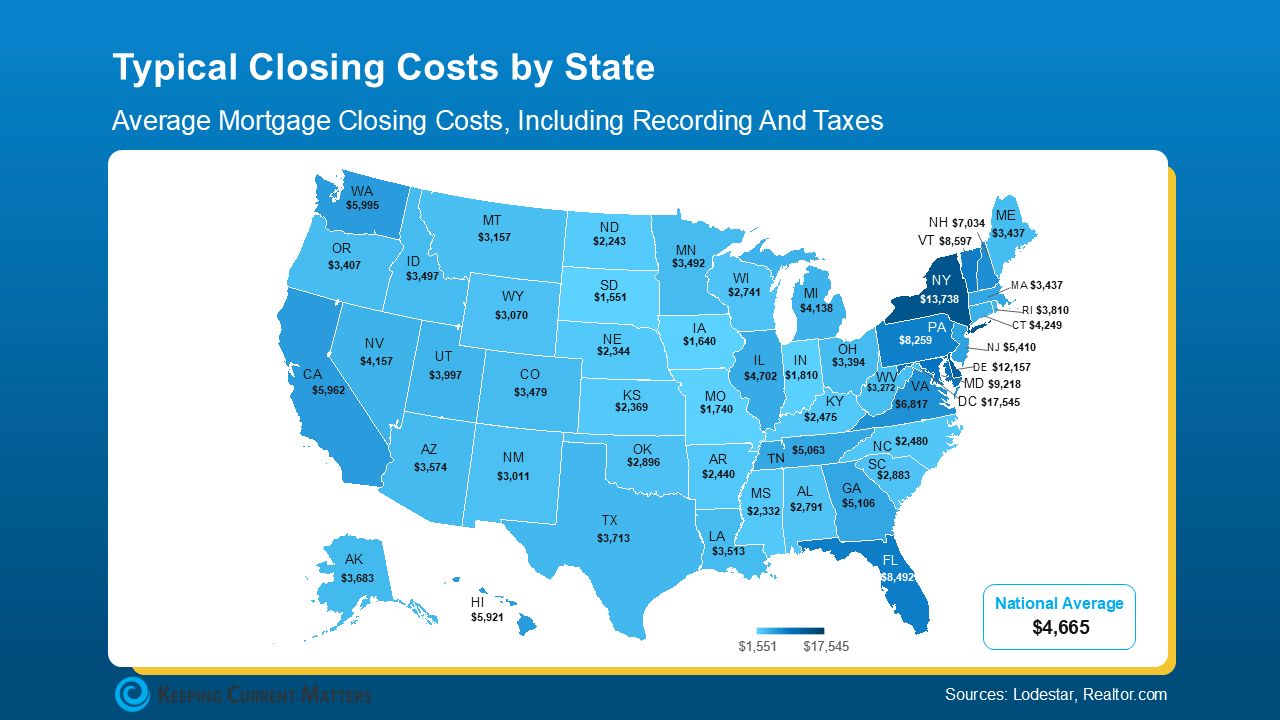

To give you a general idea, here’s a state-by-state breakdown of average closing costs right now, based on the median-priced home in each state (see map below):

As you can see on the map, closing costs vary widely. In some states, they average just $1,000–$3,000. In others, they can climb to $10,000–$15,000. That kind of difference can be a big deal, especially for first-time buyers—making it all the more important to know what to expect.

For a personalized estimate, the best step is to talk with a local agent and lender. They’ll run the numbers based on your price point, loan type, and exact location.

And if you’re wondering whether there are ways to bring that bill down, NerdWallet highlights a few helpful strategies:

- Negotiate with the seller: Ask for concessions, like a credit toward your closing costs.

- Shop for homeowner’s insurance: Compare rates and coverage before committing.

- Look into assistance programs: Certain states, professions, or neighborhoods offer support. Your agent or lender can connect you with local options.

Bottom Line

Closing costs are an essential part of the homebuying process, and they often vary far more than most people expect. Understanding what they include—and how to potentially reduce them—can make a big difference in how prepared and confident you feel when making your purchase.

That’s why it pays to connect with a trusted local agent or lender. They can walk you through typical costs in your area, provide a personalized estimate based on your price range and loan type, and help you build a budget that truly fits your goals. Taking that step now gives you clarity, confidence, and control as you move forward on your path to homeownership.

Categories

Recent Posts

GET MORE INFORMATION