What You Should Know Before Choosing an Adjustable-Rate Mortgage

If you’ve been searching for a home recently, you’ve likely noticed that affordability is still a challenge. That’s one reason more buyers are considering adjustable-rate mortgages, also known as ARMs.

Here’s what to know about how they work and whether one could be a good fit for your situation.

What Is an Adjustable-Rate Mortgage (ARM)?

Because many buyers are not as familiar with this loan option, it helps to start with a simple definition. Here’s how Business Insider explains the key difference between a fixed-rate mortgage and an adjustable-rate mortgage:

“With a fixed-rate mortgage, the interest rate stays the same for the life of the loan, which means the principal and interest portion of your monthly payment remains consistent over time. An adjustable-rate mortgage works differently. It typically starts with a fixed rate for an initial period, but after that, the rate can adjust at set intervals. If market rates rise, your payment could go up. If rates fall, your payment could go down.”

In simple terms, one loan option stays relatively consistent over the life of the mortgage, while the other can change over time, sometimes slightly and sometimes more noticeably.

With a fixed-rate loan, costs like property taxes or homeowner’s insurance may still cause your total monthly payment to shift, but the core mortgage payment usually stays stable. With an adjustable-rate mortgage, the key difference is that your monthly payment can rise or fall as the rate adjusts over time.

Why Adjustable-Rate Mortgages Are Drawing More Attention

So why are some buyers considering this route? The answer is fairly simple: the potential for lower upfront monthly costs. Business Insider explains it this way:

“Because adjustable-rate mortgages often begin with lower interest rates than fixed-rate loans, they can make homeownership feel more affordable when borrowing costs are elevated. That lower initial rate may reduce your monthly payment or increase the amount of home you can comfortably afford compared to a fixed-rate mortgage.”

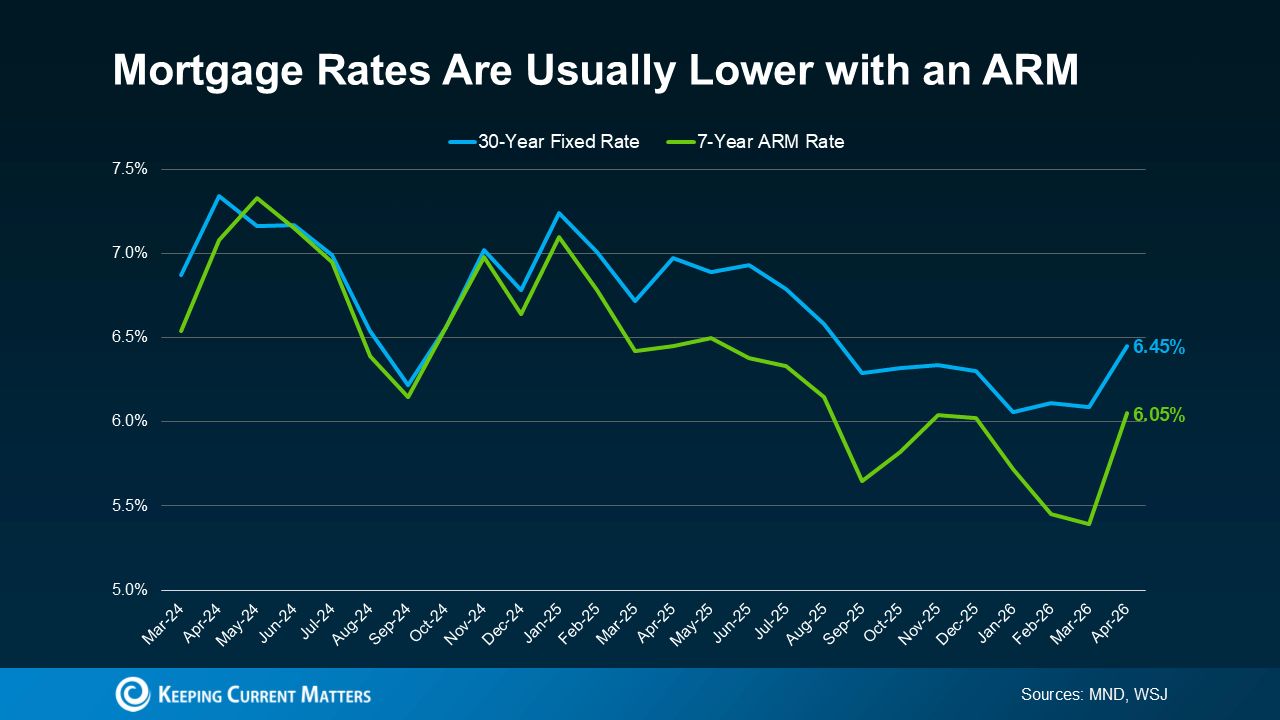

And right now, data from Mortgage News Daily and reporting from Wall Street Journal show that the starting rate on many ARMs is coming in below the rate for a traditional 30-year fixed mortgage (see graph below).

If you’re curious what that means in practical terms, Redfin reports that the average buyer could save roughly $150 per month by choosing an ARM instead of a 30-year fixed mortgage.

For some buyers, that monthly savings can make a meaningful difference.

More Buyers Are Turning to Adjustable-Rate Mortgages Today

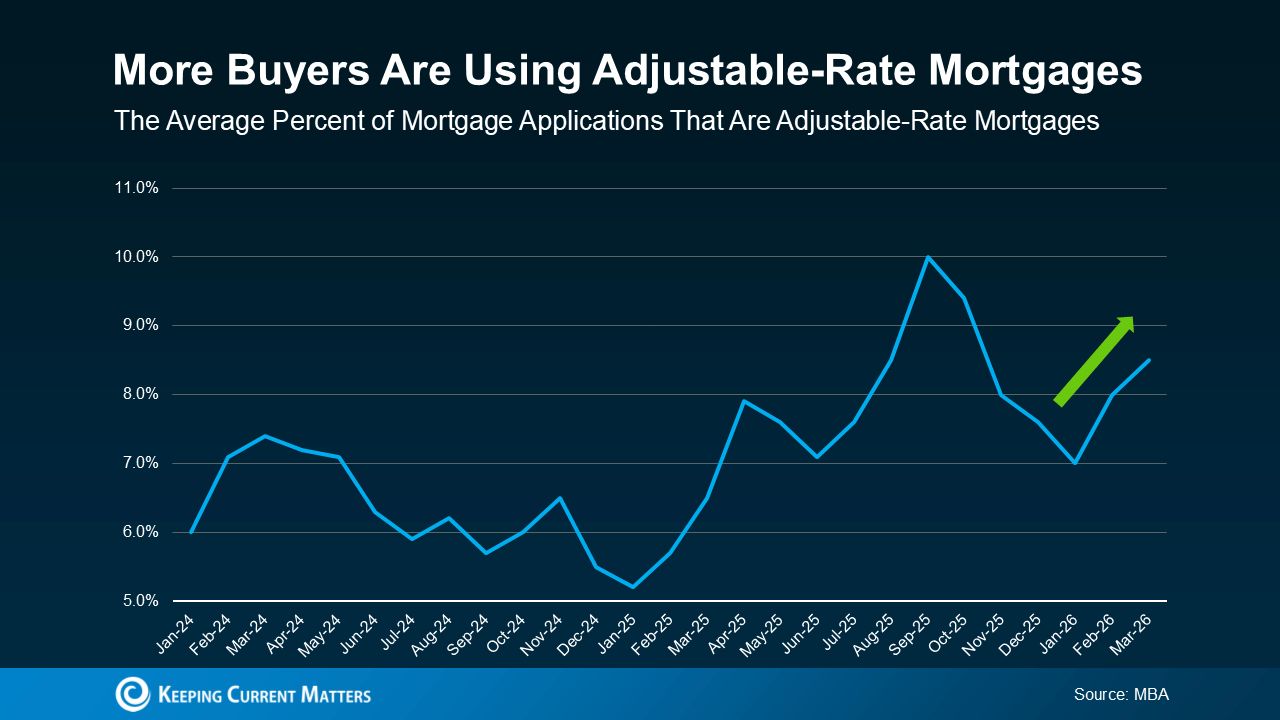

More buyers are deciding that a lower payment today is worth the possibility of changes later. Data from the Mortgage Bankers Association (MBA) shows that the share of buyers choosing ARMs has risen, particularly over the past few years (see graph below).

That does not mean ARMs are the right fit for everyone or that they have become the default choice. It simply means some buyers are using this loan option as a way to make a home purchase more manageable in today’s market.

If you remember the housing crash, it is understandable that seeing ARMs become more common again might cause some concern. But today’s adjustable-rate mortgages are very different from the ones that contributed to problems in the past.

At that time, some borrowers ended up with loans they could not realistically afford once the rate adjusted. Today, lending standards are much tighter, and borrowers are generally qualified based on whether they could still manage the payment if rates increase. So, the rise in ARM usage is not necessarily a warning sign of another housing crash. It is more a reflection of how some buyers are responding to ongoing affordability pressures.

The Trade-Off: What You Need To Consider

If you’re thinking about an adjustable-rate mortgage for your own purchase, the right choice really comes down to your personal situation and how comfortable you are with the possibility of future payment changes.

An ARM could be a good fit if you expect to move before the rate adjusts or believe your income will likely increase over time. But it’s important to weigh the trade-offs carefully.

Once the initial fixed-rate period ends, your interest rate may adjust, which means your monthly payment could go up, potentially by a noticeable amount depending on market conditions at that time.

It’s also important to remember there is no promise mortgage rates will fall later, so refinancing may not be available when you want it. That’s why it’s smart to think through your long-term plans, consider your future earning power, and talk closely with a trusted lender before deciding if an ARM is right for you.

Bottom Line

Adjustable-rate mortgages are getting more attention because they can lower monthly costs upfront and make homeownership feel more attainable in the short term. But that does not mean they are the right choice for every buyer.

What matters most is understanding how an ARM works, what the potential risks are, and whether it aligns with your financial goals and timeline. Before making a decision, it is wise to speak with a trusted lender and financial advisor so you can choose the option that best fits your situation.

{ "@context": "https://schema.org", "@type": "FAQPage", "mainEntity": [ { "@type": "Question", "name": "What is an adjustable-rate mortgage (ARM)?", "acceptedAnswer": { "@type": "Answer", "text": "An ARM is a mortgage that starts with a fixed interest rate for an initial period, after which the rate adjusts at set intervals based on market conditions — meaning your monthly payment can go up or down over time." } }, { "@type": "Question", "name": "How does an ARM differ from a fixed-rate mortgage?", "acceptedAnswer": { "@type": "Answer", "text": "With a fixed-rate mortgage, the interest rate stays the same for the life of the loan. With an ARM, the rate is fixed only for an initial period and then changes periodically based on market rates." } }, { "@type": "Question", "name": "Why are more buyers considering ARMs right now?", "acceptedAnswer": { "@type": "Answer", "text": "Because ARMs typically start with lower interest rates than fixed-rate loans, they can reduce monthly payments and make homeownership more affordable when borrowing costs are high." } }, { "@type": "Question", "name": "How much could a buyer potentially save by choosing an ARM?", "acceptedAnswer": { "@type": "Answer", "text": "According to Redfin, the average buyer could save roughly $150 per month by choosing an ARM over a 30-year fixed mortgage." } }, { "@type": "Question", "name": "Are ARMs as risky as they were before the 2008 housing crash?", "acceptedAnswer": { "@type": "Answer", "text": "No. Today's lending standards are much tighter, and borrowers are now qualified based on whether they could handle payments even if rates increase — making today's ARMs significantly safer than those from the pre-crash era." } }, { "@type": "Question", "name": "Who might an ARM be a good fit for?", "acceptedAnswer": { "@type": "Answer", "text": "An ARM may suit buyers who expect to move before the rate adjusts or who anticipate their income will increase enough to cover potential future payment increases." } }, { "@type": "Question", "name": "What are the key risks of an ARM?", "acceptedAnswer": { "@type": "Answer", "text": "Once the initial fixed period ends, your rate — and monthly payment — can rise, sometimes significantly. There's also no guarantee that rates will fall, so refinancing may not be an option when needed." } }, { "@type": "Question", "name": "What should buyers do before choosing an ARM?", "acceptedAnswer": { "@type": "Answer", "text": "They should understand how ARMs work, assess their long-term financial plans and income potential, and consult with a trusted lender and financial advisor before making a decision." } } ] }

Categories

Recent Posts

GET MORE INFORMATION