The Housing Market Isn't as Weak as the Headlines Suggest

You've probably seen plenty of headlines suggesting the housing market is struggling, higher mortgage rates, affordability challenges, and predictions of a slowdown. But the data tells a different story.

Today's market isn't 2020 or 2021, and it was never expected to be. Those years were an anomaly, driven by record-low mortgage rates, intense bidding wars, and homes selling within days. That wasn't a normal market; it was a once-in-a-generation exception.

Compared to those years, today's market may seem slower. But compared to most housing markets in modern history, it's proving to be remarkably resilient, supported by steady demand and strong fundamentals.

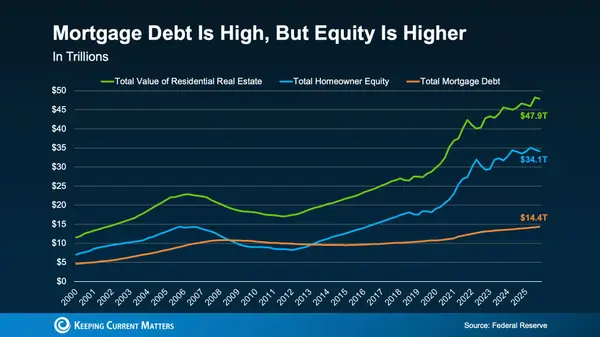

Homeowners Have Built Record Levels of Equity

One of the biggest reasons today's housing market remains resilient is the financial position of American homeowners. In 2008, homeowner equity and mortgage debt were nearly equal, according to the Federal Reserve. That left many owners with little financial cushion when home values fell, helping fuel the housing crash.

Today, the picture is dramatically different. U.S. homeowners hold roughly $35 trillion in equity, far exceeding total mortgage debt (see graph below).

That equity cushion means most homeowners aren't financially stretched or forced to sell at the first sign of hardship. Instead, they have meaningful ownership in their homes, giving them flexibility if life changes. And as home values appreciate and mortgages are paid down, that financial cushion continues to grow.

- The longer homeowners stay in their homes, the more equity they tend to build. According to Realtor.com, the average homeowner who has owned their home for five years has accumulated about $180,000 in equity. For those who've owned their home for 6–10 years, that figure exceeds $340,000.

- Meanwhile, data from ATTOM and the Census Bureau shows that roughly two-thirds of homeowners either own their home outright or have more than 50% equity.

That's not the profile of a fragile housing market. It's a nation of homeowners with the financial flexibility to sell, stay put, or make their next move from a position of strength, not necessity.

Why Low Mortgage Rates Still Matter

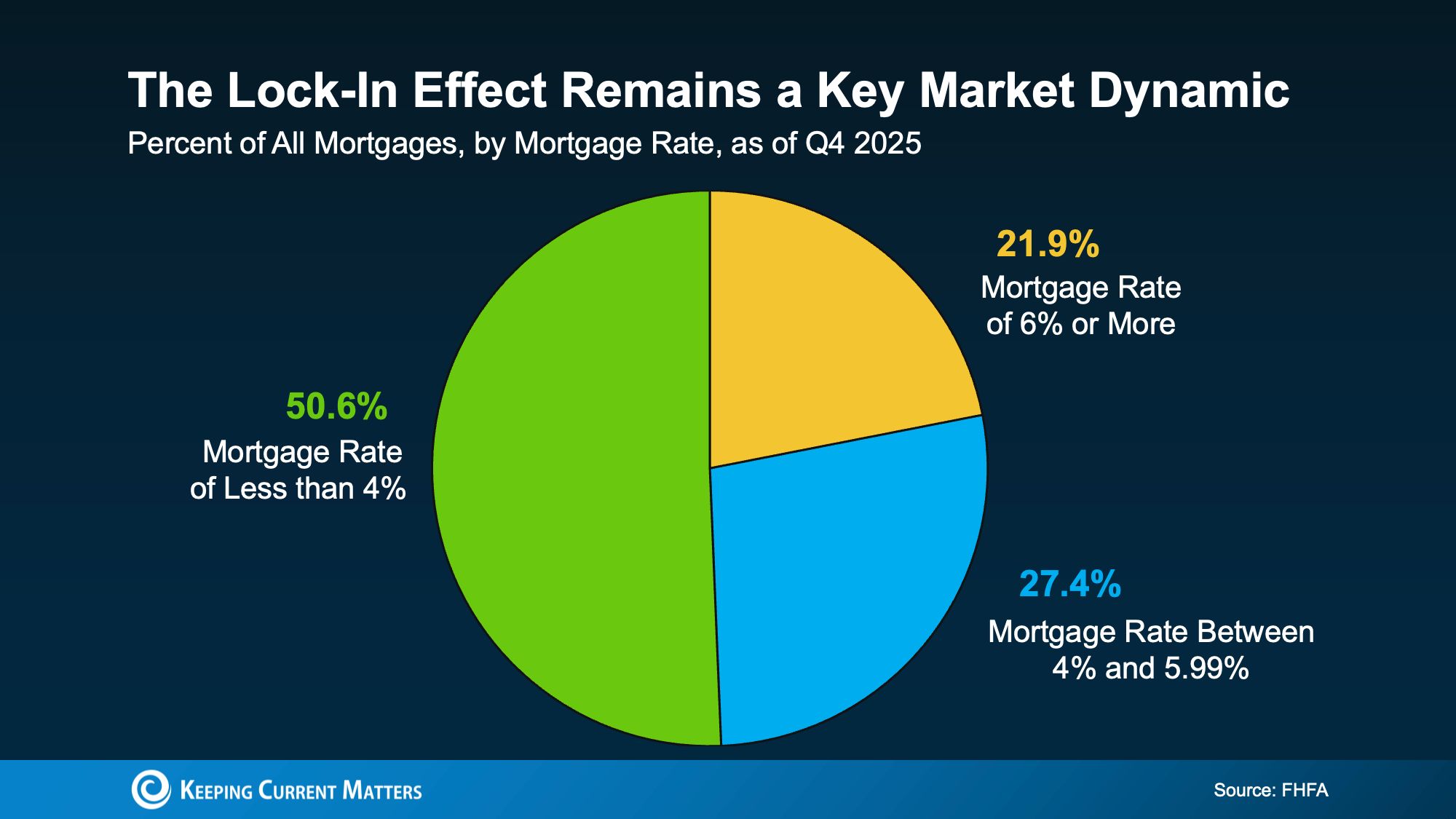

At the same time, data from the Federal Housing Finance Agency (FHFA) shows that more than half of all outstanding mortgages still have an interest rate below 4% (see graph below).

That's one of the biggest reasons inventory remains limited. Many homeowners have little incentive to give up a mortgage rate below 4% for today's higher borrowing costs. Instead, they're choosing to stay put from a position of financial strength.

That strength is reflected in the foreclosure data as well. While foreclosure activity has increased modestly, ATTOM reports it remains well below historical norms. Most homeowners have substantial equity and multiple options before foreclosure ever becomes a reality.

Home Prices Are Stabilizing, Not Crashing

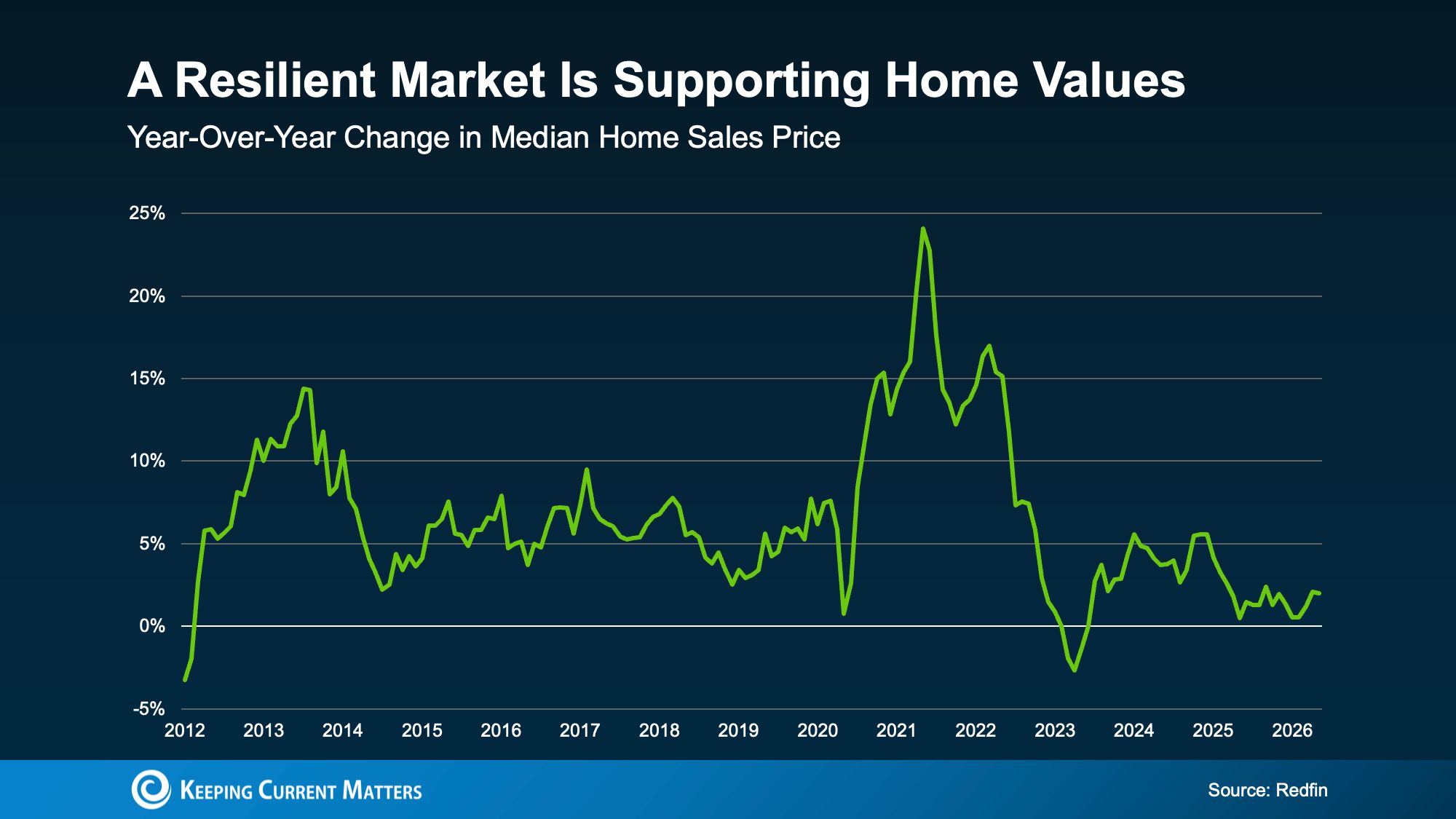

Home prices provide another sign of the market's resilience. According to Redfin, prices continue to rise nationwide, though at a more sustainable pace of about 2% year over year (see graph below).

That moderation is a healthy sign. Rather than signaling a collapse, it reflects a market returning to more sustainable conditions after the extraordinary run-up during the pandemic. As Redfin Chief Economist Daryl Fairweather notes, today's market is experiencing a normalization, not a crash, as prices and inventory gradually move back toward long-term trends.

Bottom Line

Today's housing market is fundamentally stronger than many headlines suggest. While conditions have normalized from the pandemic boom, strong homeowner equity, historically low foreclosure levels, and steady price appreciation continue to support the market.

Whether you're considering buying, selling, or simply weighing your options, understanding your local market is what matters most. A trusted real estate agent can help you evaluate your situation and make a decision that aligns with your goals—not the headlines.

Categories

Recent Posts

GET MORE INFORMATION