Down Payments Have Fallen to Their Lowest Level Since 2021

Saving for a down payment is often one of the biggest hurdles to buying a home. With affordability still a challenge, many buyers wonder whether homeownership is even within reach.

The good news? More buyers are getting into the market with smaller down payments than many people expect.

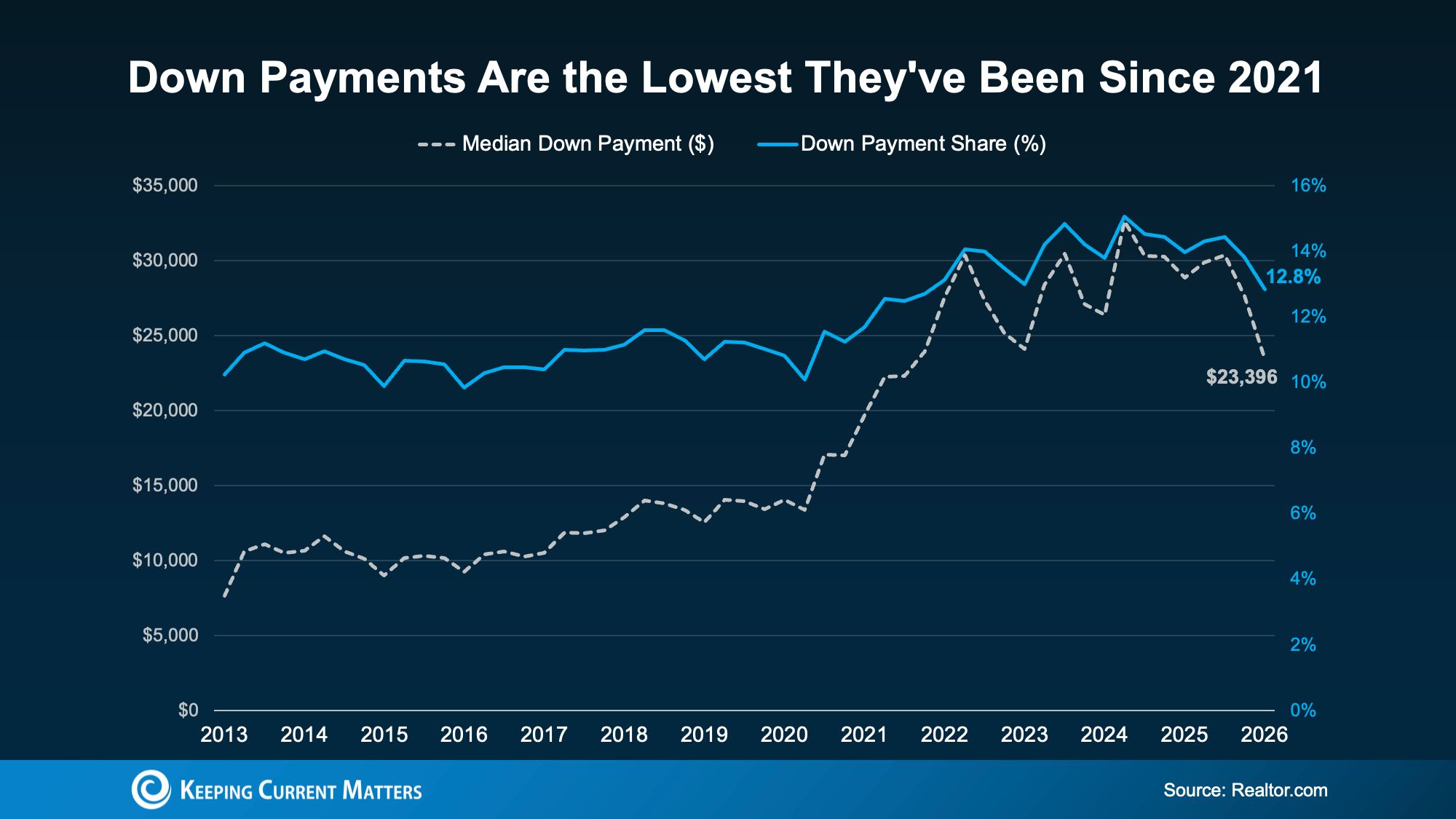

According to Realtor.com, the typical homebuyer put down about $23,400 in early 2026—roughly $5,000 less than the year before, a 19% year-over-year decline. In fact, the typical down payment is now at its lowest level since 2021, as shown in the graph below.

So, what's driving the drop in down payments, and could you buy a home with less money down as well? Here's what you need to know.

Why Buyers Are Putting Less Money Down

Several factors are contributing to today's smaller down payments:

- A more balanced housing market. With less competition than during the pandemic buying frenzy, buyers no longer feel as much pressure to make large down payments to strengthen their offers.

- Slower home price growth. Because down payments are typically based on a percentage of a home's purchase price, moderating price growth or even slight price declines in some markets—can reduce the amount buyers need upfront.

- More buyers using low-down-payment loan programs. Government-backed financing, such as FHA and VA loans, continues to gain popularity because many of these programs require little or no money down. According to Mortgage Professional America, FHA loans have accounted for more than 24% of purchase mortgages for five consecutive quarters, while VA loans recently reached their highest market share in more than a decade.

Even with today's lower down payments, buying a home still requires a meaningful upfront investment. The good news is that many buyers don't have to do it alone. Down payment assistance programs and financial gifts from family members are helping more people bridge the gap and achieve homeownership.

Down Payment Assistance You May Not Know About

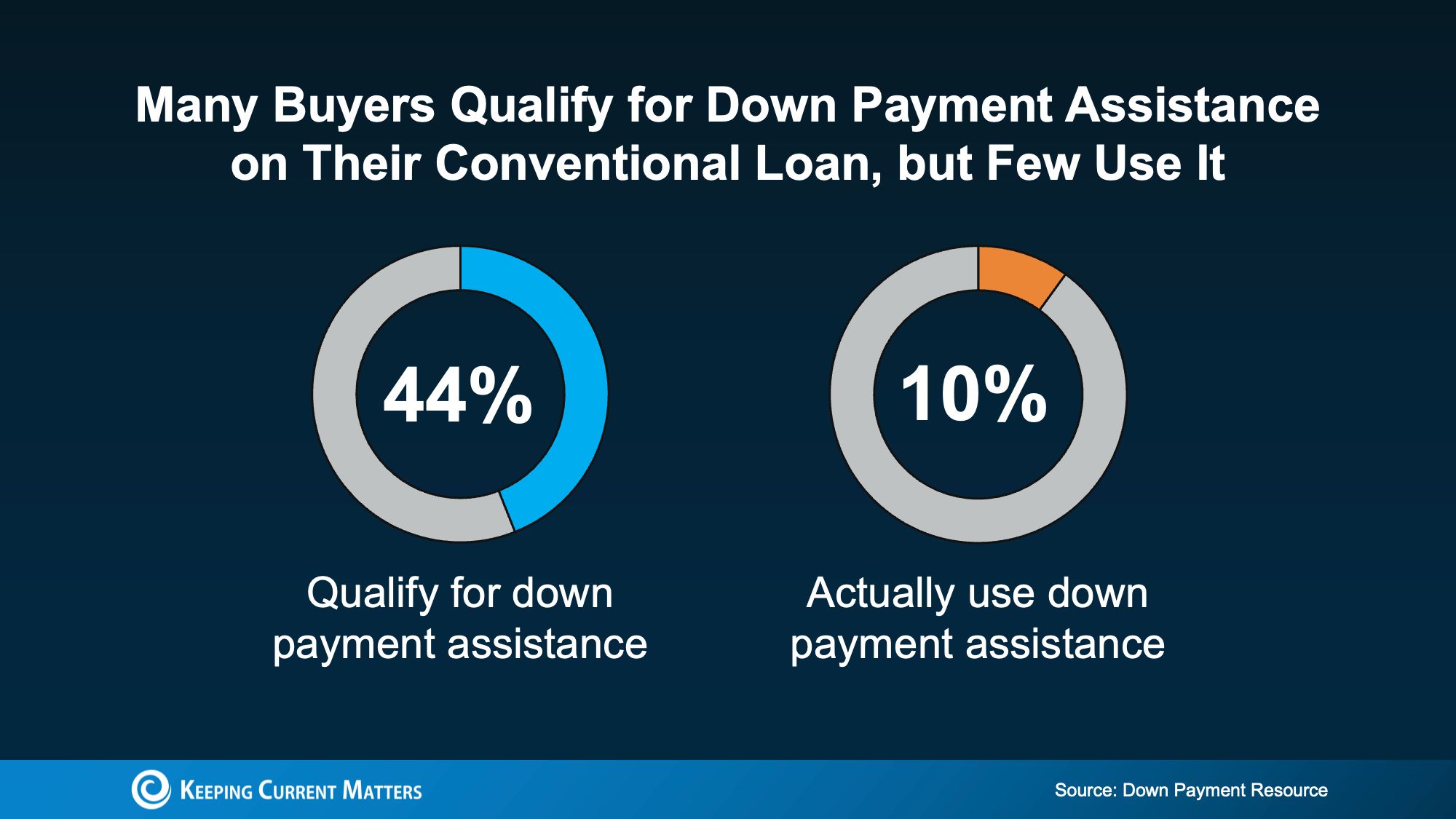

Down payment assistance is one of the most underused resources available to homebuyers. According to the Urban Institute and Down Payment Resource, nearly 44% of recent buyers in the nation's 10 largest metro areas qualified for a down payment assistance program—but many completed their home purchase without ever taking advantage of it (see chart below).

The range of options may be wider than many buyers realize. According to Down Payment Resource:

There are now more than 2,600 down payment assistance programs available nationwide. While 62% are designed for first-time buyers, 38% do not require you to be a first-time buyer—meaning you may still qualify even if you’ve owned a home before. And these programs aren’t only for low-income buyers either: 62% are available to buyers earning $100,000 or more.

A Helping Hand from Family

For many buyers, the support comes from family. According to Veterans United, nearly 6 in 10 parents have either helped—or plan to help—their children financially with the purchase of a home, making family gifts an increasingly common source of down payment funds.

When family members contribute, the money is most often used for a down payment, though many also help with closing costs or provide support that makes it easier to qualify for a mortgage.

As Chris Birk, Vice President of Mortgage Insight at Veterans United, explains, today's housing market has made family assistance less of a luxury and more of a practical way to help the next generation achieve homeownership.

If a family member is able to provide financial assistance, it could help you reach your homeownership goals sooner by making your down payment and upfront costs more manageable.

Bottom Line

Today's buyers are putting down less money than they have in years, making homeownership more attainable for many people. When you combine lower down payment requirements with available assistance programs and, in some cases, financial support from family, buying a home may be more achievable than you think.

The best way to understand what's possible is to speak with a trusted lender who can help you explore the loan and down payment options available to you.

Categories

Recent Posts

GET MORE INFORMATION