Could Co-Buying Help First-Time Buyers Get Their Foot in the Door?

For many would-be first-time buyers, affordability is the biggest roadblock. But some are finding creative ways to make homeownership possible — and co-buying is one strategy helping them do it.

The Dream Is Still There; But the Numbers Don’t Work for Everyone.

Young people haven’t abandoned the dream of homeownership — far from it. According to FirstHome IQ, owning a home is still one of the top life goals for the next generation.

The challenge? Affordability. About 73% of Gen Z and millennial buyers say the cost of homeownership is the main reason it hasn’t become a bigger priority. And the numbers reflect that reality — first-time buyers now account for just 21% of all home purchases, the lowest share since the National Association of Realtors began tracking the data in 1981.

Still, some buyers are finding ways to make homeownership happen and co-buying is becoming one of the strategies helping them break into the market.

So, What Exactly Is Co-Buying?

Co-buying means purchasing a home with another person, such as a friend, sibling, or unmarried partner. By combining incomes, sharing the down payment, and splitting monthly expenses, buyers may be able to make homeownership happen sooner.

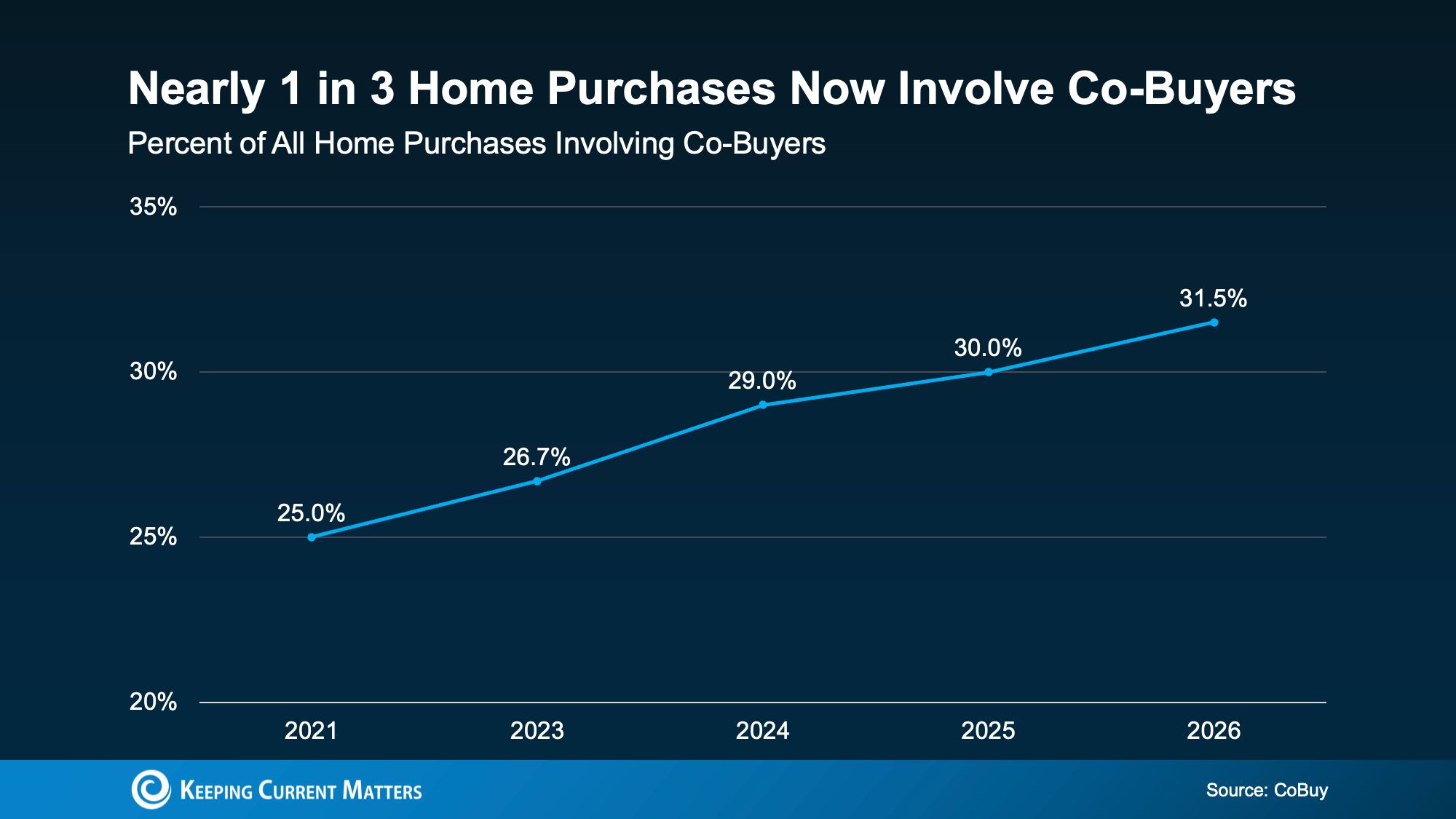

And it’s becoming more common. According to CoBuy.io, 64 million Americans now co-own a home with someone they’re not married to. In fact, 31.5% of home purchases involve co-buyers.

Why Co-Buying Can Work

According to NerdWallet, here are a few of the biggest reasons buyers are choosing to co-buy:

- A faster path to homeownership: Pooling resources with another buyer can make saving for a down payment happen much faster. Instead of waiting years to buy, some people are able to get into a home sooner and start building equity now.

- More buying power: Combining incomes may open the door to a larger home, better features, or a neighborhood that may have been out of reach financially on a solo budget.

- Better odds of qualifying for a loan: Having more than one income on the application can improve debt-to-income (DTI) ratios, which may help buyers qualify more easily with a lender.

- Lower monthly housing costs: Sharing a mortgage and other home expenses can sometimes make ownership more affordable than renting alone. It can also make ongoing costs like maintenance, repairs, and renovations easier to handle.

What Buyers Should Consider First

If you’re thinking about co-buying, it’s important to plan carefully before jumping in. This type of arrangement tends to work best when everyone involved trusts each other and has similar financial expectations and long-term goals. Before moving forward, make sure you’re aligned on key details like how expenses will be divided, who’s responsible for what, and what the plan is if one person decides to sell in the future.

That’s also why having a written co-ownership agreement is often a smart idea. It can help set clear expectations upfront, reduce misunderstandings later on, and create a roadmap for how the investment will be handled moving forward.

Bottom Line

Affordability remains one of the biggest hurdles for today’s buyers, but that doesn’t mean homeownership is out of reach. For some first-time buyers, co-buying is creating a practical path forward and helping them make the move sooner rather than later.

If you’re wondering whether co-buying could make sense for you, connecting with a local real estate agent can help you explore your options and build a strategy that fits your goals.

```html

```

Categories

Recent Posts

GET MORE INFORMATION