Should You Wait for Mortgage Rates to Drop?

Mortgage rates briefly dipped into the upper 5% range twice this year. But within just a few days, they climbed back into the low 6s. If you saw that and thought, “Great… I missed it,” you’re definitely not alone.

Many buyers are treating rates in the 5% range like a magic number — as if dropping from 6.1% to 5.99% suddenly changes everything. And psychologically, it does feel different.

But here’s the part most people never actually stop to calculate.

The Payment Difference May Surprise You

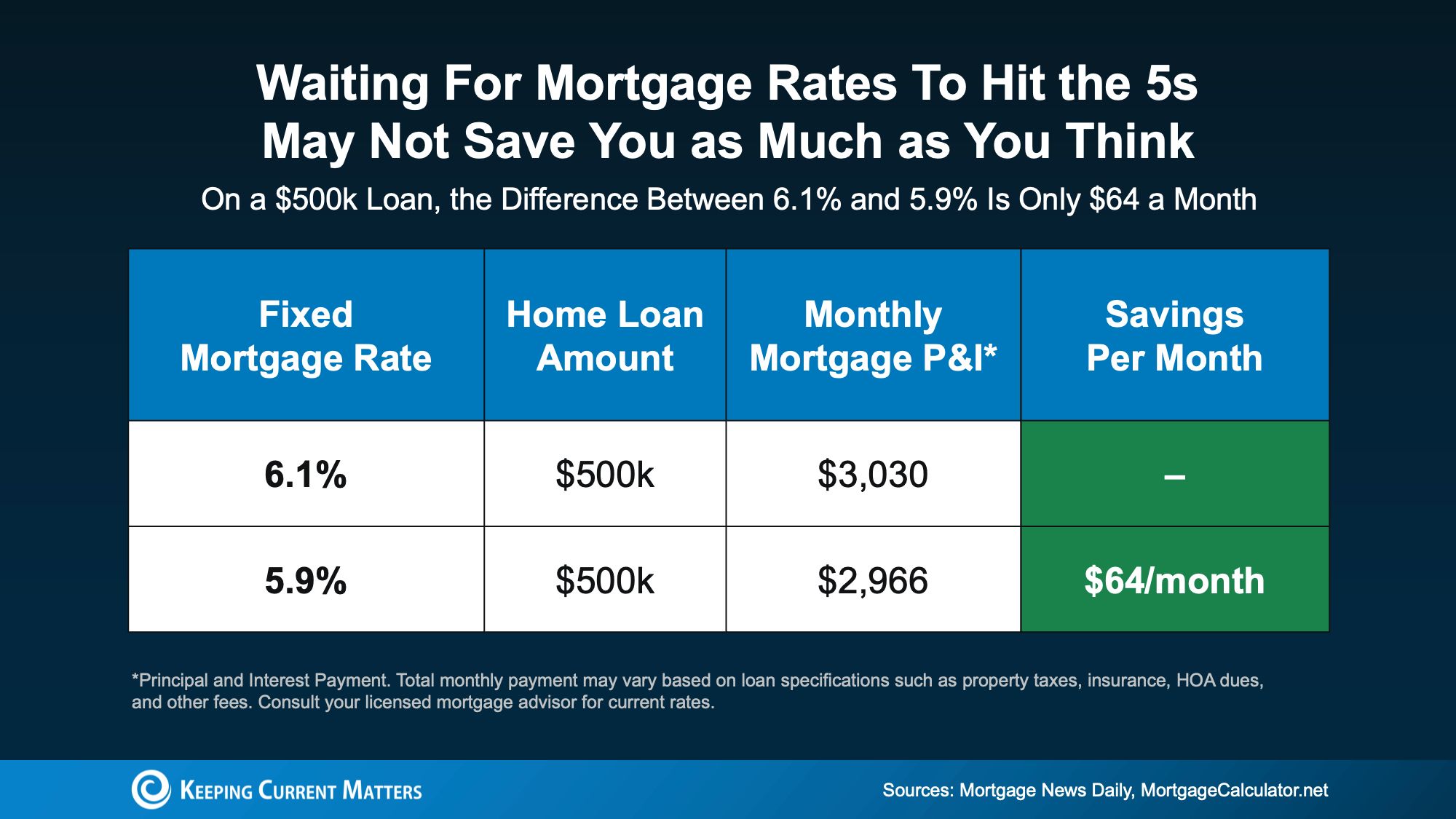

Let’s say you’re financing a $500,000 home loan. At 6.1%, the principal and interest payment is roughly $3,030 per month. If the rate drops to 5.9%, that payment falls to about $2,966 per month.

That’s only about a $64 difference per month.

Not $300.

Not $500.

Sixty dollars.

Take a moment to let that sink in.

Yes, over time that extra $64 a month does add up. But it’s nowhere near the dramatic change many buyers picture when they say they’re “waiting for rates in the 5s.”

Seeing a 5 at the start of your rate can feel significant psychologically. Financially, though, the difference may be so small you barely notice it in the long run.

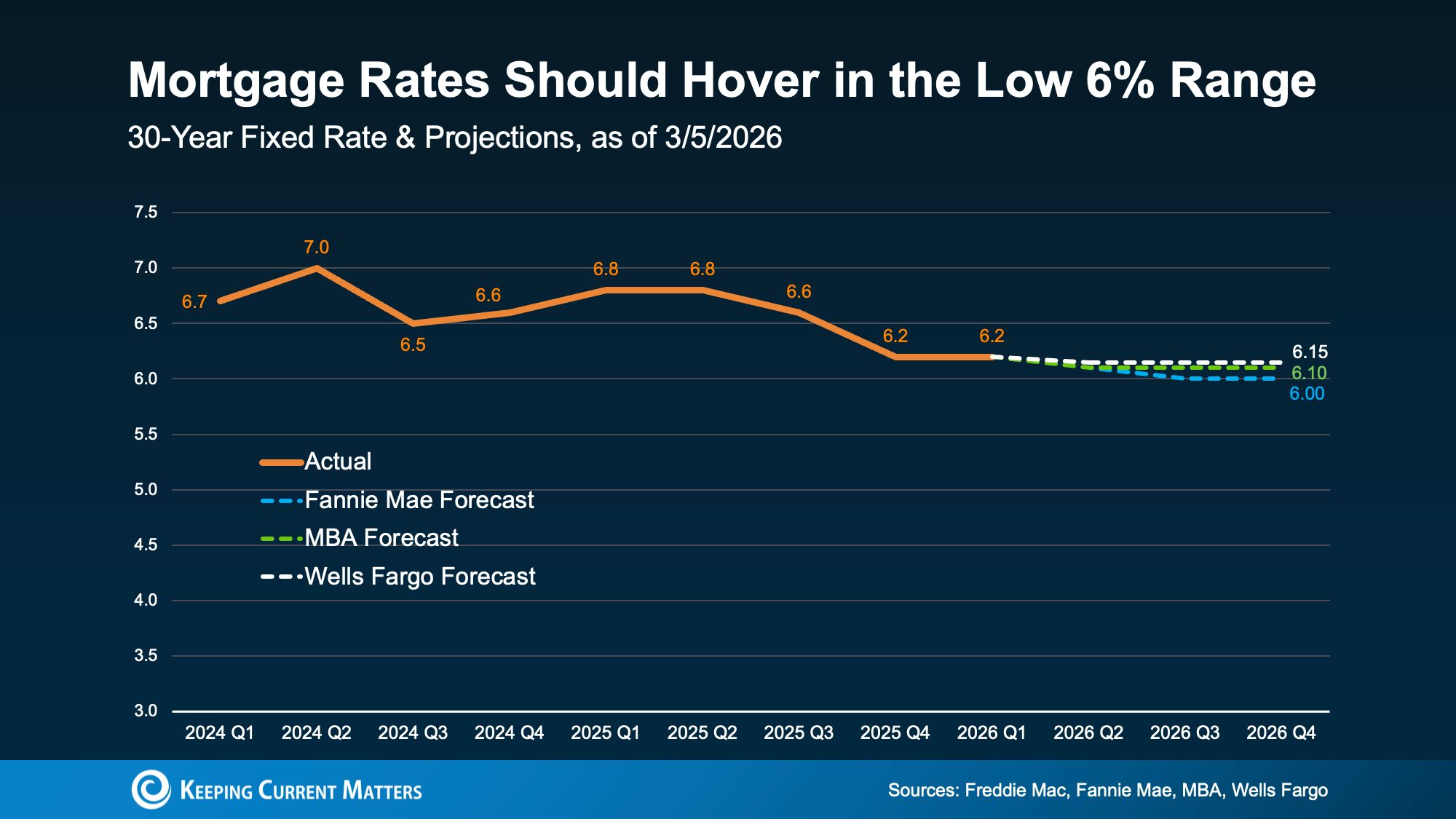

Experts Don’t Expect a Major Rate Drop

Another important factor to consider: most housing economists aren’t predicting a sustained return to the 5% range anytime soon. While rates may fluctuate and occasionally dip into the high 5s, the broader outlook is for mortgage rates to hover in the low 6% range this year rather than remain in the 5s or fall much further.

While it’s certainly possible, the reality is that waiting for a significant drop may not deliver the payoff many buyers are hoping for.

The Bigger Question to Ask

Instead of asking, “Did I miss rates in the 5s?” a more useful question is: “Does today’s payment work for my budget?”

If the monthly payment fits comfortably and the home checks the boxes you’re looking for, the difference between 6.1% and 5.9% probably won’t be the deciding factor. It may play a role, but it shouldn’t be the only thing driving the decision.

And remember, mortgage rates aren’t permanent. If rates fall meaningfully in the future, refinancing is always an option. But you can’t refinance a home you never purchased.

Waiting Can Feel Safe, But It Isn’t Always Strategic

It’s completely natural to want the best possible rate—everyone does. But many buyers overestimate how much a move into the high 5% range would actually change things in today’s market.

It’s also important to remember that rates have already come down. A year ago they were in the 7% range. Today, they’re hovering in the low 6s. For many buyers, that one-percentage-point improvement that’s already happened is the real game changer.

If you put your plans on hold when rates were higher, now may be a good time to revisit the numbers. Not because rates are “perfect,” but because the monthly payment may be more manageable than you expect, even with rates in the low 6s.

Before assuming your opportunity has passed, take another look at the numbers.

You might find it never actually went away.

Bottom Line

If you’ve been waiting on the sidelines for mortgage rates to reach the “magic” 5% range, that strategy may not deliver the payoff many buyers expect.

Connect with a trusted agent or lender to review the numbers based on your price range—you may find that today’s payments are already within reach.

{ "@context": "https://schema.org", "@type": "FAQPage", "mainEntity": [ { "@type": "Question", "name": "Many buyers seem fixated on mortgage rates dropping into the 5% range. How significant is that psychological threshold?", "acceptedAnswer": { "@type": "Answer", "text": "The 5% mark carries a strong psychological pull because seeing a 5 at the start of a rate feels very different than seeing a 6. But while that perception is understandable, the financial reality is often less dramatic. On a $500,000 loan, the monthly principal and interest payment difference between 6.1% and 5.9% is only about $64 per month, which is far less than many buyers expect when they talk about waiting for rates in the 5s." } }, { "@type": "Question", "name": "Can you break down the actual payment difference between 6.1% and 5.9% on a $500,000 loan?", "acceptedAnswer": { "@type": "Answer", "text": "At 6.1%, the principal and interest payment on a $500,000 loan is approximately $3,030 per month. At 5.9%, that payment drops to around $2,966 per month, a difference of just $64. While that amount does add up over time, it is far from the $300 to $500 monthly savings many buyers imagine when they decide to wait for rates to fall into the 5% range." } }, { "@type": "Question", "name": "What are housing economists currently projecting for mortgage rates?", "acceptedAnswer": { "@type": "Answer", "text": "Most housing economists are not forecasting a sustained return to the 5% range in the near term. The broader consensus is that mortgage rates are more likely to hover in the low 6% range for the foreseeable future. While occasional dips into the high 5s are possible, buyers expecting a prolonged and meaningful rate decline may end up waiting much longer than anticipated." } }, { "@type": "Question", "name": "What's a better question for buyers to ask themselves instead of \"Did I miss rates in the 5s?\"", "acceptedAnswer": { "@type": "Answer", "text": "A more strategic question is, \"Does today's payment fit my budget?\" Rather than anchoring a decision to a specific interest rate number, buyers should focus on whether the current monthly payment is manageable and whether the home meets their needs. A small difference in rate may matter, but it usually should not be the only factor driving the decision." } }, { "@type": "Question", "name": "What role does refinancing play in the decision to buy now versus wait?", "acceptedAnswer": { "@type": "Answer", "text": "Refinancing gives buyers an important option if rates drop meaningfully after they purchase. Homeowners can refinance into a lower rate and potentially reduce their monthly payment. Buyers who remain on the sidelines do not have that flexibility, because you cannot refinance a home you never bought or capture the equity, appreciation, and stability that can come with ownership during the waiting period." } }, { "@type": "Question", "name": "How much have mortgage rates already improved compared to a year ago?", "acceptedAnswer": { "@type": "Answer", "text": "Mortgage rates have already improved meaningfully. About a year ago, many rates were in the 7% range, while today they are hovering in the low 6s. That roughly one-percentage-point improvement has already reduced monthly payments in a real way for many buyers, and for some, that shift is more impactful than waiting for a much smaller drop from 6.1% to 5.9%." } }, { "@type": "Question", "name": "Is waiting for a lower rate always a bad strategy?", "acceptedAnswer": { "@type": "Answer", "text": "Not always. Waiting can make sense if current payments genuinely do not fit a buyer's budget or if there is a strong reason to believe a meaningful rate drop is likely. The challenge is that many buyers overestimate how much a modest rate reduction will change their monthly payment, or assume a major drop is right around the corner without clear evidence. In that case, the opportunity cost of waiting can outweigh the benefit." } }, { "@type": "Question", "name": "What should buyers do if they've been waiting on the sidelines?", "acceptedAnswer": { "@type": "Answer", "text": "The most practical next step is to revisit the numbers using today's mortgage rates and the price range of homes you are considering. Many buyers find that the payment is more manageable than they expected. If the monthly cost works for your budget, there may be less reason to keep waiting. Talking with a trusted real estate agent or lender to run a personalized analysis is a smart place to start." } } ] }

Categories

Recent Posts

GET MORE INFORMATION