The Truth Behind Today’s Foreclosure Headlines

You’ve probably come across headlines claiming that foreclosures are increasing, and for many people, that immediately brings back memories of 2008. That reaction makes sense. The housing crash left a lasting impression, and a lot of homeowners and buyers understandably don’t want to see history repeat itself.

But today’s market is very different from what we saw back then. Here’s the important context that the headlines often leave out.

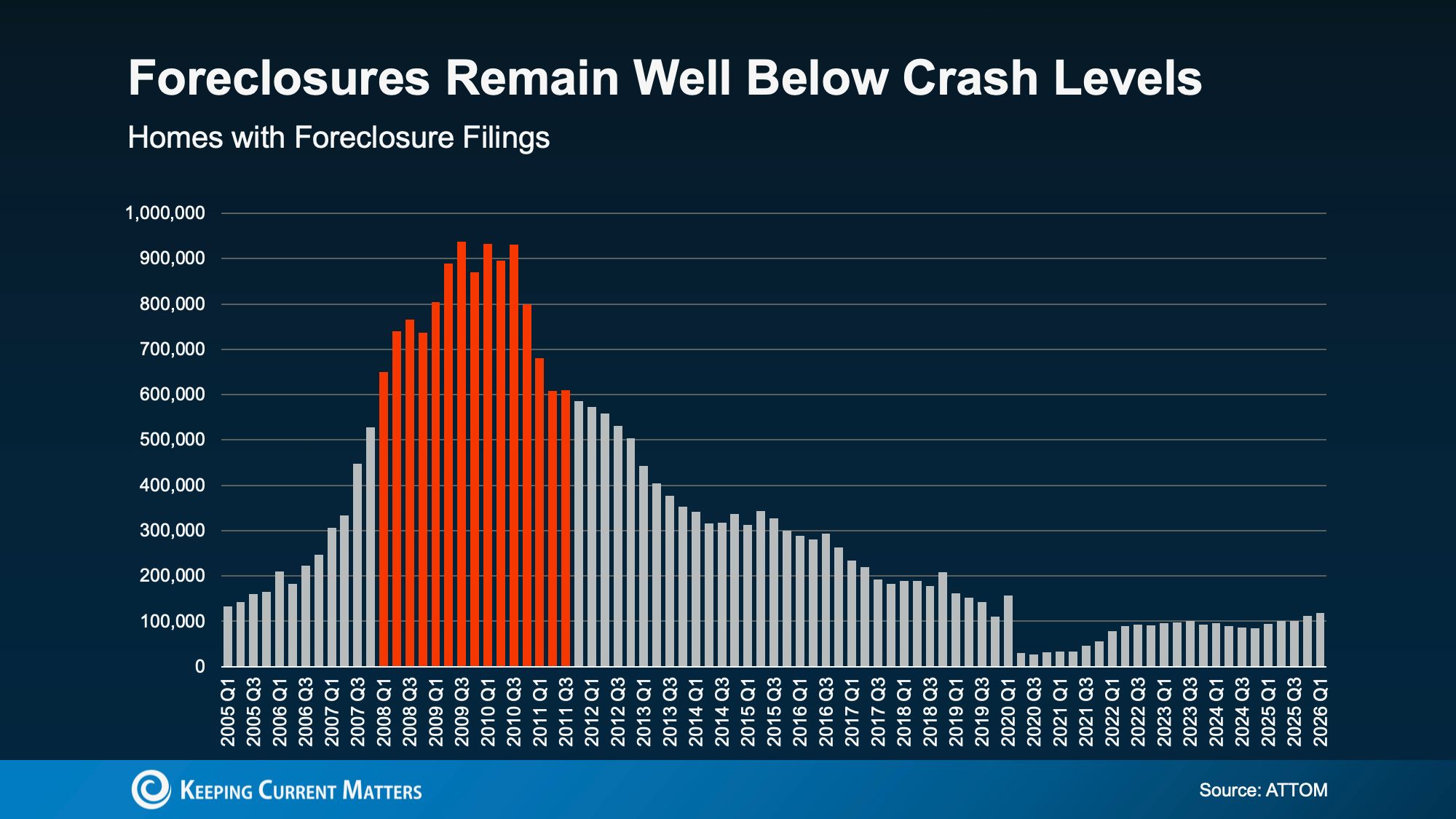

Foreclosures Are Up, But Still Far Below Historic Levels

Yes, foreclosure filings are up 26% from last year, according to ATTOM, and they’ve increased for 5 straight quarters. That’s a trend worth watching. But the full story isn’t as alarming as the headlines make it sound.

What we’re really seeing is the market moving back toward a more normal pace.

Here’s an important detail about this chart: the unusually low foreclosure numbers in 2020 and 2021 were not “normal” market conditions. During the pandemic, the government introduced foreclosure moratoriums to help homeowners stay in their homes. Those years were the exception — not the standard.

A better comparison is to look at 2017, 2018, and 2019, when the housing market was operating under more typical conditions. Even compared to those years, today’s foreclosure levels are still lower. That’s why the current increase doesn’t point to a housing crash. It’s much more reflective of the market returning to normal patterns. (See graph below.)

While today’s numbers are getting closer to pre-pandemic levels, they’re still below historical norms. And just look at what was happening around 2008. Even with the recent increase, we’re nowhere near those levels. This is a market returning to normal, not heading toward a crisis.

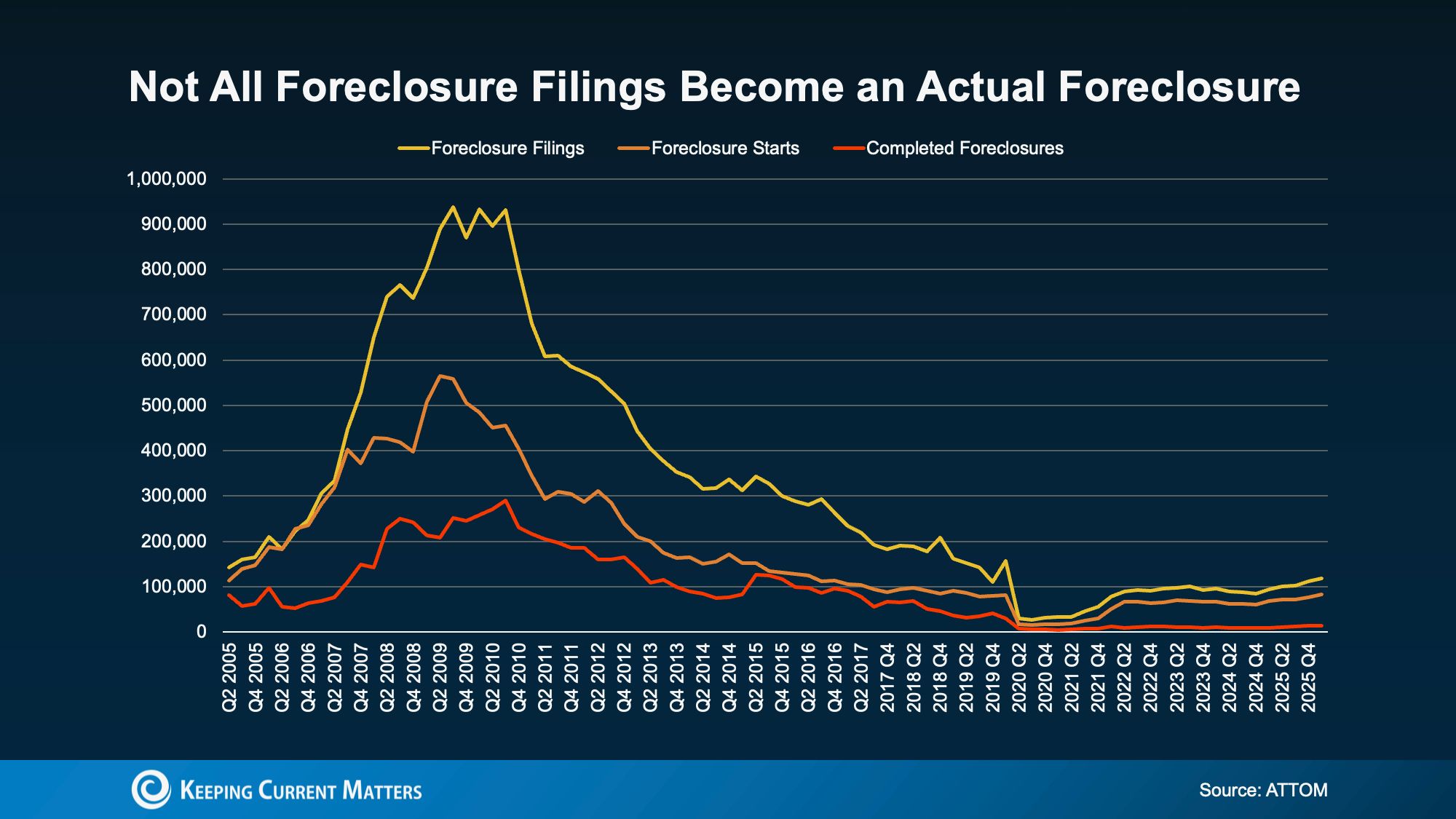

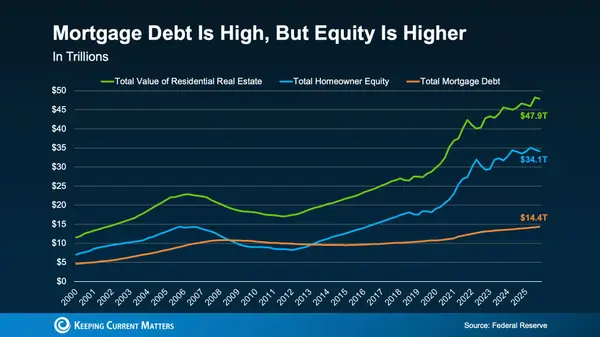

Why Homeowner Equity Changes the Foreclosure Conversation

Many of today’s foreclosure filings likely won’t end in an actual foreclosure. One major reason is that homeowners today are in a very different financial position than they were in 2008 — largely because of the amount of equity they’ve built.

According to Cotality, the average homeowner currently has around $295,000 in home equity. During the 2008 housing crash, many homeowners were underwater, meaning they owed more than their homes were worth. In many cases, selling wasn’t even an option, leaving foreclosure as one of the only paths forward.

Today, the situation looks very different. If a homeowner has enough equity to cover what they owe and the costs of selling, they may be able to sell the home, pay off the debt, avoid major damage to their credit, and possibly still walk away with money.

That’s a completely different reality than many homeowners faced during the last crash, and it’s one of the biggest reasons we’re unlikely to see foreclosures spiral the way they did back then.

Here’s how to look at the graph below. It uses ATTOM foreclosure data dating back to 2005 and breaks the numbers into three categories:

- The yellow line shows total foreclosure filings.

- The orange line shows foreclosure starts, meaning the foreclosure process has officially begun.

- The red line shows completed foreclosures — the cases where a homeowner actually lost the home.

Notice how the red line remains much lower than the other two? That gap tells the bigger story. Many homeowners who enter the foreclosure process are still able to avoid losing their home by finding another solution before foreclosure is completed.

And a major reason for that is the amount of equity many homeowners have today. That means a large portion of the filings we’re seeing now may never result in an actual foreclosure.

If You’re Falling Behind, You May Still Have Options

Maybe you’ve fallen behind on payments or you’re worried about what the future holds. That can feel overwhelming, but missing a payment or two does not automatically mean you’re going to lose your home.

In many cases, lenders would rather help homeowners find a solution than move forward with foreclosure. Foreclosure is expensive and time-consuming for banks as well. Because of that, many lenders are open to working out repayment plans, offering temporary forbearance, or modifying loan terms to make monthly payments more manageable over time.

The most important thing is to communicate with your lender as early as possible. The sooner you reach out, the more options you’re likely to have available. In some states — especially those with non-judicial foreclosure processes — timelines can move quicker than many homeowners realize. Acting early gives you and your lender more flexibility to work toward a solution.

And if selling the home ends up being the better option, a real estate agent can help you understand your home’s value and whether selling could help you move forward financially.

Bottom Line

While foreclosure filings have been increasing, they’re still sitting at relatively low levels compared to historical norms. More importantly, today’s housing market is fundamentally different from what we experienced during the 2008 crash. One of the biggest reasons is the amount of equity homeowners have built over the past several years.

That equity gives many homeowners more flexibility and more options if financial challenges arise — whether that means working with a lender, restructuring payments, or selling before foreclosure ever becomes necessary. So while the headlines may sound alarming, the overall market conditions today tell a much different story than they did during the last housing crisis.

Categories

Recent Posts

GET MORE INFORMATION