Adjustable-Rate Mortgages Aren’t for Everyone—Are They Right for You?

If you’ve been house hunting recently, you’ve probably felt the pressure of today’s mortgage rates. Combine that with rising home prices, and it’s no surprise that more buyers are exploring alternative loan options to make their budgets work. One loan type seeing a resurgence? Adjustable-rate mortgages (ARMs).

Now, if the term "ARM" brings back memories of the 2008 housing crash, you're not alone. But today’s ARMs are different—and much safer.

Back then, many buyers were approved for loans they couldn’t actually afford once the rates adjusted. Today, lenders are far more cautious. They evaluate whether you can still handle the loan if the rate goes up, offering a stronger layer of protection.

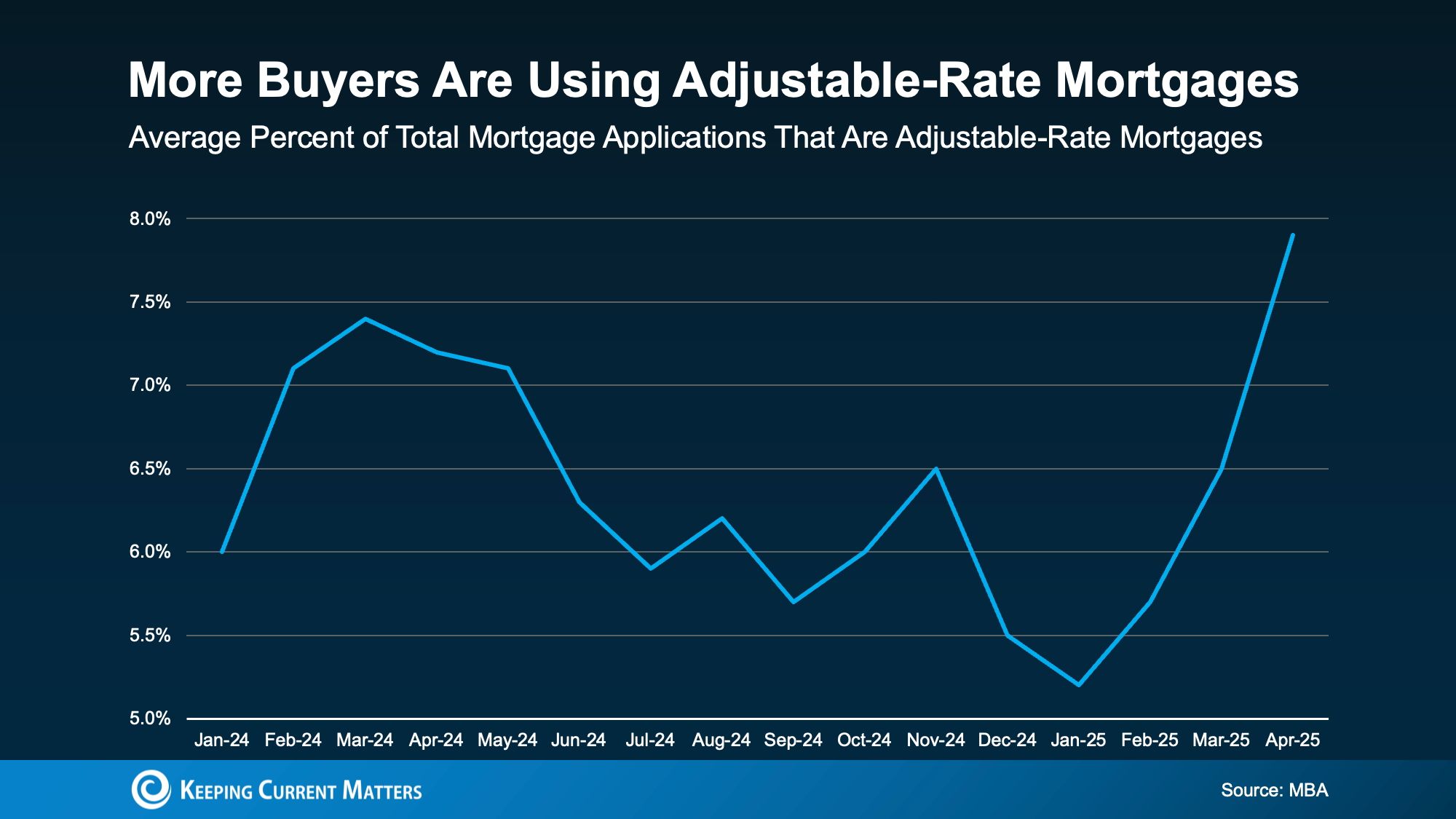

So, don’t panic—ARMs aren’t a red flag. They’re a reflection of buyers getting creative in a challenging market. Just take a look at this trend from the Mortgage Bankers Association (MBA): more buyers are choosing ARMs right now (see graph below).

Adjustable-Rate Mortgages: Worth a Second Look? ARMs aren’t for everyone—but in the right situation, they can offer meaningful benefits.

How an ARM Works

Business Insider breaks it down simply:

“With a fixed-rate mortgage, your interest rate stays the same for the life of the loan, keeping your monthly payments predictable. An adjustable-rate mortgage starts off with a fixed rate for a few years, but after that, the rate adjusts periodically—going up or down based on market conditions.”

While fixed-rate mortgages provide stability (aside from changes in taxes or insurance), ARMs can introduce more variability after the initial period ends.

Why Some Buyers Are Opting for ARMs

The main draw? A lower starting interest rate. Business Insider explains:

“Because ARM rates are typically lower than fixed mortgage rates, they can help buyers find affordability when rates are high. That lower rate can reduce your monthly payment—or boost your buying power.”

In a high-rate environment, that flexibility can make a difference.

The Risk to Consider

But there’s a tradeoff. Barron’s adds:

“Adjustable-rate loans offer a lower initial rate, but recalculate after a period. That can be a win if rates fall—or if you sell before the adjustment kicks in. But if rates rise and you’re still in the home, your payment could jump.”

That’s why ARMs work best when you have a shorter time horizon or expect rates to drop. But because market forecasts are never a sure thing, it’s critical to assess your risk tolerance.

Before committing, have a candid conversation with your lender and financial advisor. They’ll help you weigh your options and see if an ARM aligns with your financial game plan.

Bottom Line

For the right buyer, adjustable-rate mortgages can offer meaningful advantages—especially in today’s high-rate environment. But they’re not a universal solution. What matters most is understanding how they function, carefully weighing the potential benefits and risks, and thinking through whether this type of loan aligns with your short- and long-term financial goals. That’s why it’s so important to have a conversation with a trusted lender and financial advisor. They can help you explore the numbers, assess your comfort with future rate changes, and make sure you’re choosing the mortgage strategy that truly supports your situation.

Categories

Recent Posts

GET MORE INFORMATION