Homeownership: The Long-Run Payoff You Don’t Want to Miss

Renting often seems cheaper and easier than buying — especially today. No surprise repairs, no tax bills, no stress over mortgage rates. You pay your rent and keep moving.

But here’s what gets overlooked: rent doesn’t build anything for your future. Every payment disappears the moment it’s sent, while homeowners grow their net worth simply by holding onto their property. So if you’re questioning whether buying is still worth it, the long-term numbers tell a much clearer story than most people realize.

Renting vs. Owning: What Your Money Actually Does

Here’s the real distinction: rent checks disappear the moment they’re paid. But when you own, a portion of every payment comes back to you as equity — the wealth you build as your home appreciates and your mortgage balance drops.

So even if renting feels cheaper today, there’s a major long-term tradeoff: you’re not building anything for your future. And that long-term gap is bigger than most people realize.

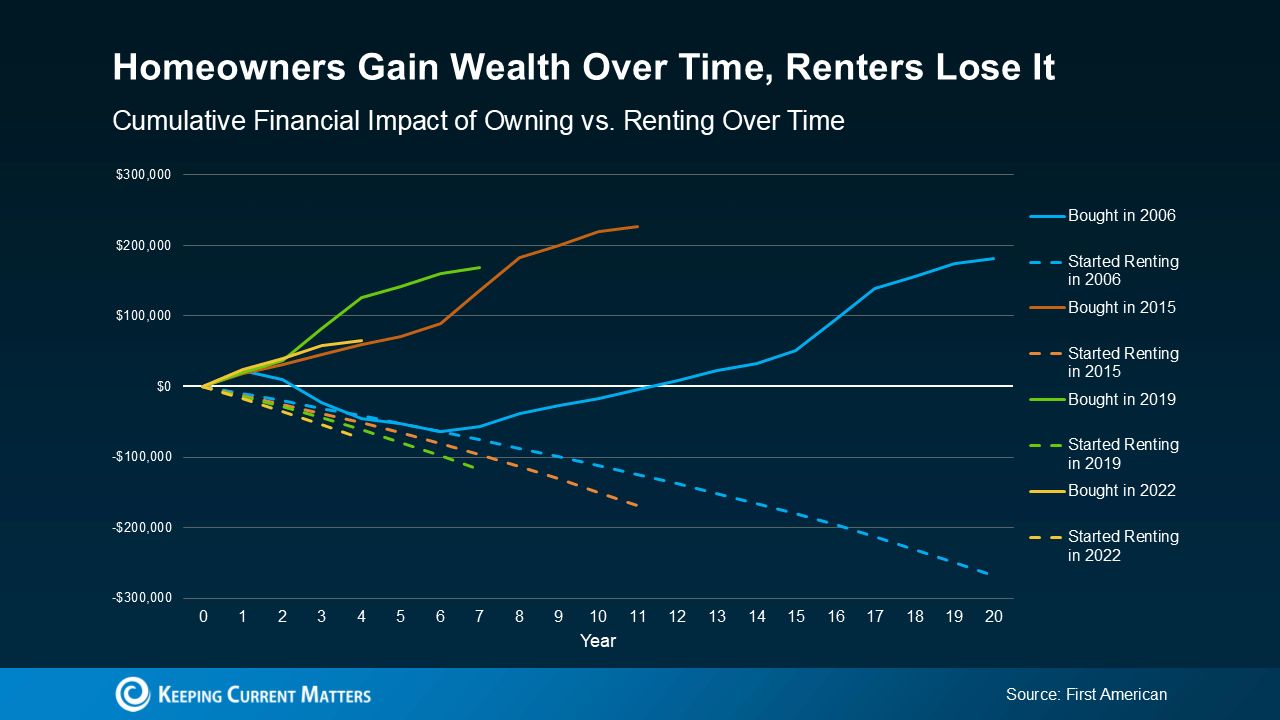

First American recently looked at the long-term financial outcomes of renting versus owning. They reviewed every major cost — mortgage payments, taxes, insurance, repairs, and maintenance — and compared them to the equity homeowners gain from rising home values and paying down their loans. They ran the analysis across multiple starting points to see whether the pattern held:

- 2006: the beginning of the housing bubble

- 2015: a full decade back

- 2019: just before the pandemic reshaped the market

- 2022: when mortgage rates spiked

And the results were the same every time: renters lost money in the long run, while homeowners steadily built wealth.

Take a look at the numbers. Each color reflects a different starting year, and the solid lines show how a homeowner’s net worth grows the longer they stay in their home. The dotted line shows the renter’s path — steady payments with no return. Over time, homeowners build equity, while renters continue putting money in without getting anything back.

The bottom line: owning a home builds wealth over time — renting doesn’t.

Homeowners consistently come out ahead, even after accounting for insurance, repairs, and property taxes. That held true across every time frame First American reviewed.

Renters, on the other hand, paid out month after month without gaining any long-term financial upside — no matter which period you compare.

Buying isn’t always the cheaper move in the short run, but the longer you own, the more dramatically the wealth gap widens.

Affordability Is Finally Starting To Turn a Corner

If you’re thinking, “Buying still feels tough right now,” you’re not wrong — the last few years have been rough for buyers. But the landscape is beginning to shift. Mortgage rates have inched down, price growth is cooling, and wages have been rising. Zillow even reports that typical monthly payments are a bit more manageable than they were this time last year — not a huge drop, but enough to matter.

Buying isn’t suddenly effortless. But it is more achievable than it was just a few months ago — and the long-term payoff remains hard to ignore.

Bottom Line

Bottom Line: Renting can seem cheaper in the moment, but ownership is what actually builds long-term wealth. And with affordability finally easing a bit, the door to buying may be wider than it looks. If you’re wondering what your next step could be, reach out to a local agent who can walk you through your options — no pressure, just clarity.

{ "@context": "https://schema.org", "@type": "FAQPage", "mainEntity": [ { "@type": "Question", "name": "Why is homeownership considered a “wealth-generating engine” compared to renting?", "acceptedAnswer": { "@type": "Answer", "text": "Studies from First American show that across multiple starting points—2006, 2015, 2019, and 2022—owners who stayed in their homes long enough saw their equity gains exceed the total costs of owning, including mortgage payments, taxes, insurance, and maintenance. Renters over those same periods simply paid out housing costs with no offsetting equity, meaning their money never turned into an asset that could grow their net worth." } }, { "@type": "Question", "name": "What does it actually mean that “rent checks disappear, but mortgage payments build equity”?", "acceptedAnswer": { "@type": "Answer", "text": "When you rent, 100% of your monthly payment goes to the landlord and is gone forever, even if you stay for years. As an owner, part of each mortgage payment reduces your principal balance, so over time you own more of the home—and if values rise, that ownership stake (equity) becomes an increasingly valuable part of your net worth." } }, { "@type": "Question", "name": "How big is the wealth gap between homeowners and renters today?", "acceptedAnswer": { "@type": "Answer", "text": "Recent research finds the median net worth of homeowners is around the high hundreds of thousands of dollars, while renters’ median net worth is closer to just over ten thousand dollars, a gap of roughly 30–40 times or more in some reports. That difference is largely driven by home equity—the accumulated value of owning property over many years." } }, { "@type": "Question", "name": "Does buying at a “bad time” (like 2006) still pay off in the long run?", "acceptedAnswer": { "@type": "Answer", "text": "Yes—First American’s analysis shows even buyers who purchased near the peak of the 2006 housing bubble ultimately generated well over six figures in cumulative wealth from equity if they held on through the downturn and recovery. While prices fell initially, the long stretch of post-2012 appreciation more than offset the early losses and ownership costs over time." } }, { "@type": "Question", "name": "What about buyers who purchased more recently, like 2015, 2019, or 2022?", "acceptedAnswer": { "@type": "Answer", "text": "A buyer who purchased a median-priced home in 2015 has accumulated roughly the mid–$200,000 range in equity gains, with renters in that same period paying well into six figures in rent instead. Even 2019 and 2022 buyers—those who bought just before and during the rate spike—have built tens to hundreds of thousands in wealth, while comparable renters simply incurred ongoing rent with no asset to show for it." } }, { "@type": "Question", "name": "How long does someone usually need to stay in a home for ownership to beat renting?", "acceptedAnswer": { "@type": "Answer", "text": "Analyses from groups like the Urban Institute suggest that over holding periods of a decade or more, homeownership tends to deliver strong annualized returns, often in the high single or double digits when including tax benefits. There may be shorter windows where renting temporarily looks cheaper, but over typical tenure lengths of around 8–10 years, owning has historically come out ahead in most markets." } }, { "@type": "Question", "name": "If owning includes taxes, insurance, and repairs, how can it still win financially?", "acceptedAnswer": { "@type": "Answer", "text": "The key is that equity growth from price appreciation and principal paydown often outweighs these ownership costs over time. First American’s rent-vs-own models explicitly include maintenance, taxes, and insurance, yet still show that staying in the home long enough typically leads to net positive wealth gains for owners compared with renters." } }, { "@type": "Question", "name": "Isn’t renting safer because there’s no risk of home prices falling?", "acceptedAnswer": { "@type": "Answer", "text": "Renting avoids price volatility, but it also locks you into 100% outflow with no chance to benefit from long-term appreciation or loan paydown. Historical data shows that while there are down cycles, U.S. home values over long horizons have tended to rise, making ownership a key source of net worth growth for many households." } }, { "@type": "Question", "name": "What about flexibility—doesn’t renting make more sense if someone might move soon?", "acceptedAnswer": { "@type": "Answer", "text": "Renting can be a better short-term fit if you expect to move within just a few years, because transaction costs like closing fees and agent commissions can eat into short holding-period gains. Once you cross into a longer ownership horizon—often 7–10 years or more—the benefits of equity growth typically outweigh those upfront costs." } }, { "@type": "Question", "name": "Is homeownership still realistic with today’s prices and rates?", "acceptedAnswer": { "@type": "Answer", "text": "Affordability has been challenging, but it is improving: recent Zillow data shows typical monthly mortgage payments have dipped compared with a year ago, helped by slightly lower rates, more price cuts, and wage growth outpacing home value gains. That shift is modest, not dramatic, but it’s enough to expand what some buyers can afford and to open up options that were out of reach just months earlier." } }, { "@type": "Question", "name": "How are mortgage rate changes affecting what buyers can afford now?", "acceptedAnswer": { "@type": "Answer", "text": "As rates have pulled back from their recent peaks, the same buyer can sometimes qualify for more home at a similar monthly payment, or secure a noticeably lower payment on the same price. Even relatively small declines in rates can translate into meaningful monthly savings over a 30-year loan, especially when combined with seller concessions or modest price softening." } }, { "@type": "Question", "name": "If ownership is so powerful, why do so many people feel stuck renting?", "acceptedAnswer": { "@type": "Answer", "text": "High prices, elevated (though easing) mortgage rates, and limited savings for down payments have made the entry point to ownership harder, particularly for first-time buyers. Many renters also carry other debts that strain their budgets, making it tougher to qualify, even though ownership is often the main path to breaking that cycle and building wealth." } }, { "@type": "Question", "name": "How can a renter start turning housing costs into long-term wealth?", "acceptedAnswer": { "@type": "Answer", "text": "The first step is to analyze your local rent-versus-own numbers with a knowledgeable agent or lender, looking at realistic purchase prices, current rates, and expected time in the home. From there, building a targeted savings plan for your down payment and closing costs helps you shift from paying someone else’s mortgage to building your own equity." } }, { "@type": "Question", "name": "What should someone focus on if they are close but not quite ready to buy?", "acceptedAnswer": { "@type": "Answer", "text": "Key priorities typically include improving credit, reducing high-interest debt, and building cash reserves so that you qualify for better loan programs and feel comfortable with ongoing costs like taxes and maintenance. At the same time, keeping an eye on local affordability trends and inventory with a local agent ensures you can move quickly when the numbers finally line up in your favor." } }, { "@type": "Question", "name": "Why is working with a local real estate agent so important in this decision?", "acceptedAnswer": { "@type": "Answer", "text": "Local agents understand neighborhood-level price trends, rent levels, and competition, which allows them to model realistic rent-versus-own scenarios instead of relying on national averages. They can also connect you with trusted lenders, identify homes that fit both your lifestyle and budget, and help you navigate negotiations so that your first step into ownership sets you up for long-term wealth, not stress." } } ] }

Categories

Recent Posts

GET MORE INFORMATION