Why Homeowners Are Finally Walking Away From Their Low Rates

If you’re like many homeowners, you’ve probably had the thought: “I’d move… but I don’t want to lose my 3% rate.” Totally understandable — that rate has been a huge financial win.

But here’s the truth: a great rate doesn’t fix a home that no longer fits your life. Needs change. Families grow. Priorities shift. And sometimes your home has to evolve with you. And you’re far from alone — plenty of homeowners are making that same decision right now.

The Lock-In Effect Is Finally Loosening Up

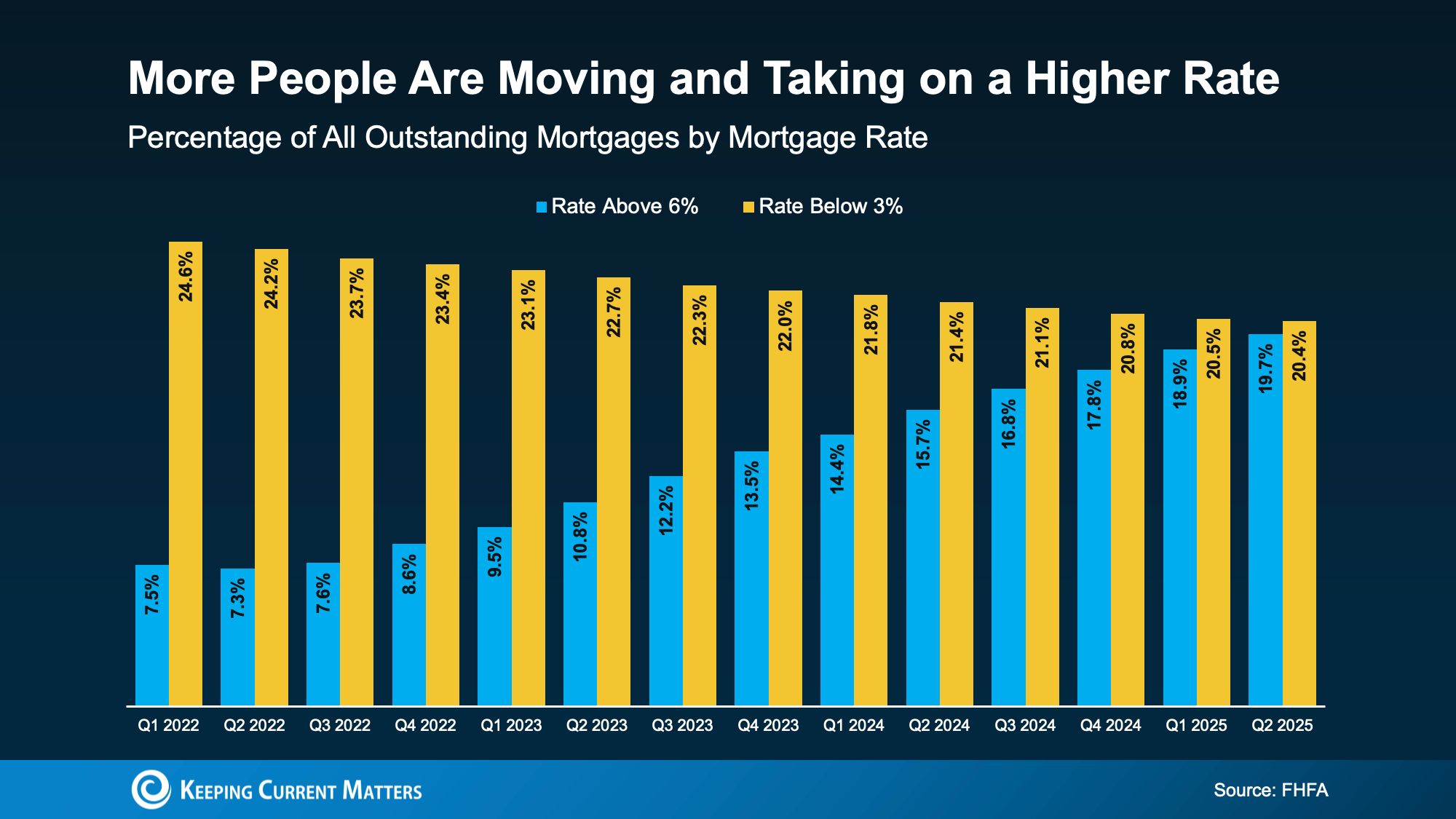

For a long time, homeowners felt stuck — a dynamic experts call the lock-in effect. It happens when people stay put simply to avoid swapping their low rate for a higher one on their next home. But new data from the Federal Housing Finance Agency (FHFA) shows that grip is starting to ease.

The share of homeowners holding rates below 3% (the yellow in the chart) is gradually shrinking as more owners decide to make a move. And while some of the buyers taking on 6%+ rates are first-timers, we’re also seeing more current homeowners step into that higher-rate category (the blue) as they trade up, downsize, or relocate.

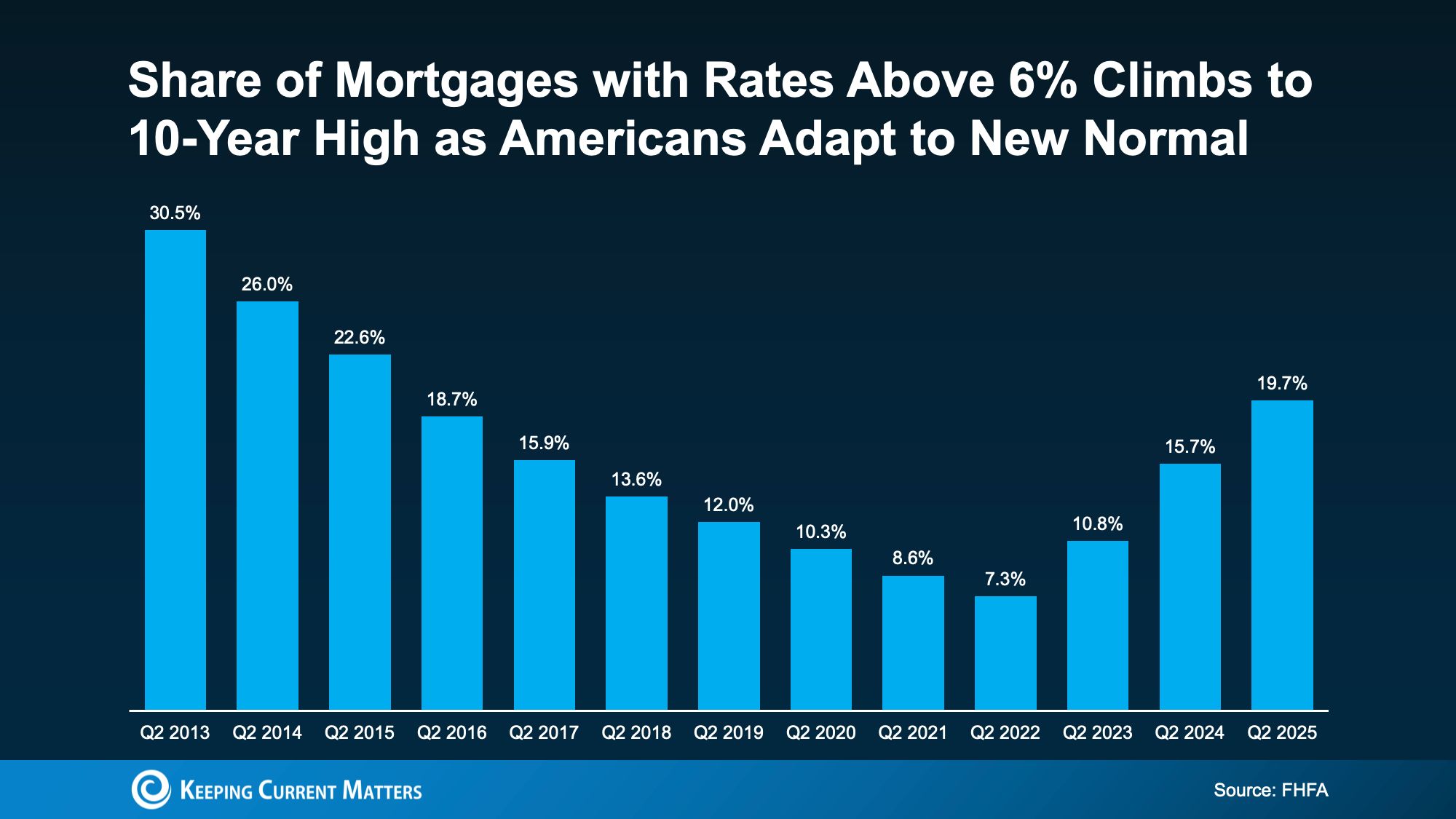

And while the change might look subtle, it’s actually significant. The share of mortgages with rates above 6% just reached a 10-year high (see chart below). That tells us more homeowners are accepting today’s rates as the new normal — and moving forward anyway.

Why Are More Homeowners Moving Even If It Means Taking On a Higher Rate?

Because life doesn’t wait. Families expand, jobs evolve, priorities change — and the home that once worked perfectly may not work anymore, regardless of how great the old rate was. And that’s okay. As Chen Zhao, Head of Economic Research at Redfin, puts it:

“More homeowners are choosing to move, even if it means letting go of their low mortgage rate. Life keeps moving — new jobs, growing families, downsizing, or wanting a different community. Those real-life needs are starting to outweigh the benefit of holding onto a rock-bottom rate.”

First American sums up these major life drivers as the 5 Ds:

- Diplomas: As education and careers progress, earning power grows — and so does the desire for a home that reflects that next chapter.

- Diapers: A growing family often means outgrowing your current space. A new baby can quickly make a once-comfortable home feel too tight.

- Divorce: Whether a relationship is ending or beginning, major life changes can create the need for a new place to start fresh.

- Downsizing: When the kids move out or priorities shift, a smaller home with less upkeep can offer more freedom and simplicity.

- Death: Losing a loved one can make you rethink what matters most — including being closer to family and support.

Whatever your reason, here’s the real consideration: your low rate is valuable, but staying put could mean keeping your life on pause. And maybe that’s no longer serving you.

Realtor.com reports that nearly two out of three potential sellers have been thinking about moving for more than a year. That’s a long time to delay your plans, your needs, and your family’s future.

So maybe the real question isn’t “Should I move?” It’s: “How much longer am I willing to stay in a home that no longer fits my life?”

And with rates already easing off their recent highs — and projected to soften more in 2026 — the combination of improving affordability and your real-life needs might be the sign you’ve been waiting for.

Bottom Line

Here’s a more polished, slightly longer (about 1% more) conclusion that lands with clarity and confidence:

Life doesn’t pause for the perfect rate — and maybe you don’t need to either. With mortgage rates already down from their peak and expected to ease a bit more in 2026, making a move might be more achievable than it seems. If you’re curious about what’s realistic in today’s market, start by connecting with a local agent and lender who can walk you through your options and help you see the full picture.

Categories

Recent Posts

GET MORE INFORMATION