Is Renting a Home Currently a Better Option Than Buying?

You might have come across recent news reports suggesting that renting is currently more economical than buying a home. While this may hold true in certain areas when considering monthly payments alone, there's a crucial factor being overlooked in these calculations: home equity. Let's delve into the significant influence equity can wield and why it's imperative to take it into account when making your decision.

Data Behind the Headlines

The chart provided utilizes national data sourced from Realtor.com for median mortgage payment and from the National Association of Realtors (NAR) for median mortgage payments to contrast the two choices. As depicted in the graph, particularly if your space requirements are modest, renting can prove to be more cost-effective on a monthly basis.

However, if your preference is for a property featuring two bedrooms, the margin between the median rent and the median mortgage payment begins to narrow, potentially becoming more manageable. The median monthly mortgage payment stands at $2,040, while the median monthly rent for two-bedroom accommodations is $1,889, resulting in a disparity of approximately $151 per month. Yet, it's essential to consider the impact of equity in this comparison.

The Game-Changing Impact of Home Equity

When you choose to rent, your monthly payments solely contribute to covering your housing expenses and your landlord's overhead. Therefore, apart from potentially saving a bit more each month and the possibility of receiving your rental deposit upon moving out, the funds allocated to housing expenditures vanish permanently.

Purchasing a home entails your monthly mortgage payment serving dual purposes: covering your shelter needs while also functioning as an investment. This investment flourishes through accruing equity as you consistently make mortgage payments, gradually reducing your home loan balance. Furthermore, your equity receives a supplementary boost with the typical appreciation of home values.

To provide a more vivid perspective on the rapid accumulation of equity, consider the following data. Fannie Mae and Pulsenomics routinely release findings from the Home Price Expectations Survey (HPES) every quarter. This survey engages over 100 economists, real estate professionals, as well as investment and market strategists, seeking their insights into the future trajectory of home prices. According to the most recent release, these experts anticipate a continued upward trend in home prices over the next five years.

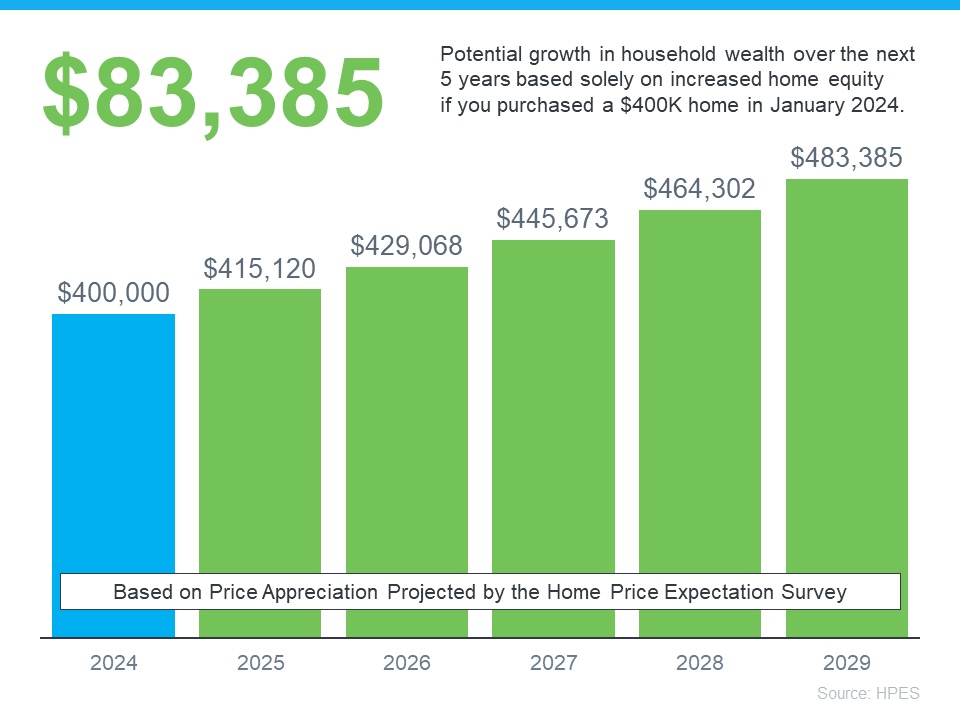

Below, you'll find an illustration demonstrating the growth of equity based on the forecasts provided by the HPES (refer to the graph).

Consider this scenario: you acquired a home for $400,000 earlier this year, intending to reside there for an extended period. According to the HPES forecasts, staying put for five years could potentially yield a household wealth increase of more than $83,000 as your home appreciates in value.

Let's compare this to renting, utilizing the previously mentioned median rent:

Although you might enjoy some savings on your monthly expenses by renting at present, you'll forego the opportunity to build equity.

So, what's the key message here? The decision between renting and buying depends greatly on your individual financial situation. If the numbers don't align in your favor, it's not advisable to pursue buying. However, if you're financially prepared and capable, recognizing the significance of equity might be the determining factor that convinces you that buying is the wiser choice for your long-term goals.

Bottom Line

Ultimately, purchasing a home offers a distinct advantage that renting simply cannot offer: the opportunity to build equity. If you're interested in leveraging the potential long-term appreciation of home prices, consider consulting with a local real estate agent to explore your available options.

Categories

Recent Posts

GET MORE INFORMATION