Rising Home Insurance Costs: What Buyers Need to Know

Buying a home is one of the biggest financial decisions you’ll ever make, and homeowner’s insurance plays a critical role in protecting that investment. Think of it as your financial safety net. According to NerdWallet, a standard policy typically helps by:

- Covering repair and rebuilding costs if your home is damaged by fire, storms, or other covered events—even covering a full rebuild in some cases.

- Protecting your personal belongings, including furniture, electronics, jewelry, and clothing, if they’re stolen or damaged.

- Providing liability coverage to help pay for medical bills or legal expenses if someone is injured on your property.

That protection brings peace of mind—but rising costs are making it more expensive than ever.

What’s Driving Higher Home Insurance Premiums

Several factors are contributing to rising insurance premiums today. But at a basic level, higher costs come down to two main issues, according to the Insurance Research Council.

Severe weather and natural disasters are happening more frequently, leading to a growing number of claims. At the same time, construction materials and labor have become more expensive. As a result, when insurers need to repair or rebuild damaged homes, they’re facing much higher costs—costs that ultimately get passed on to homeowners.

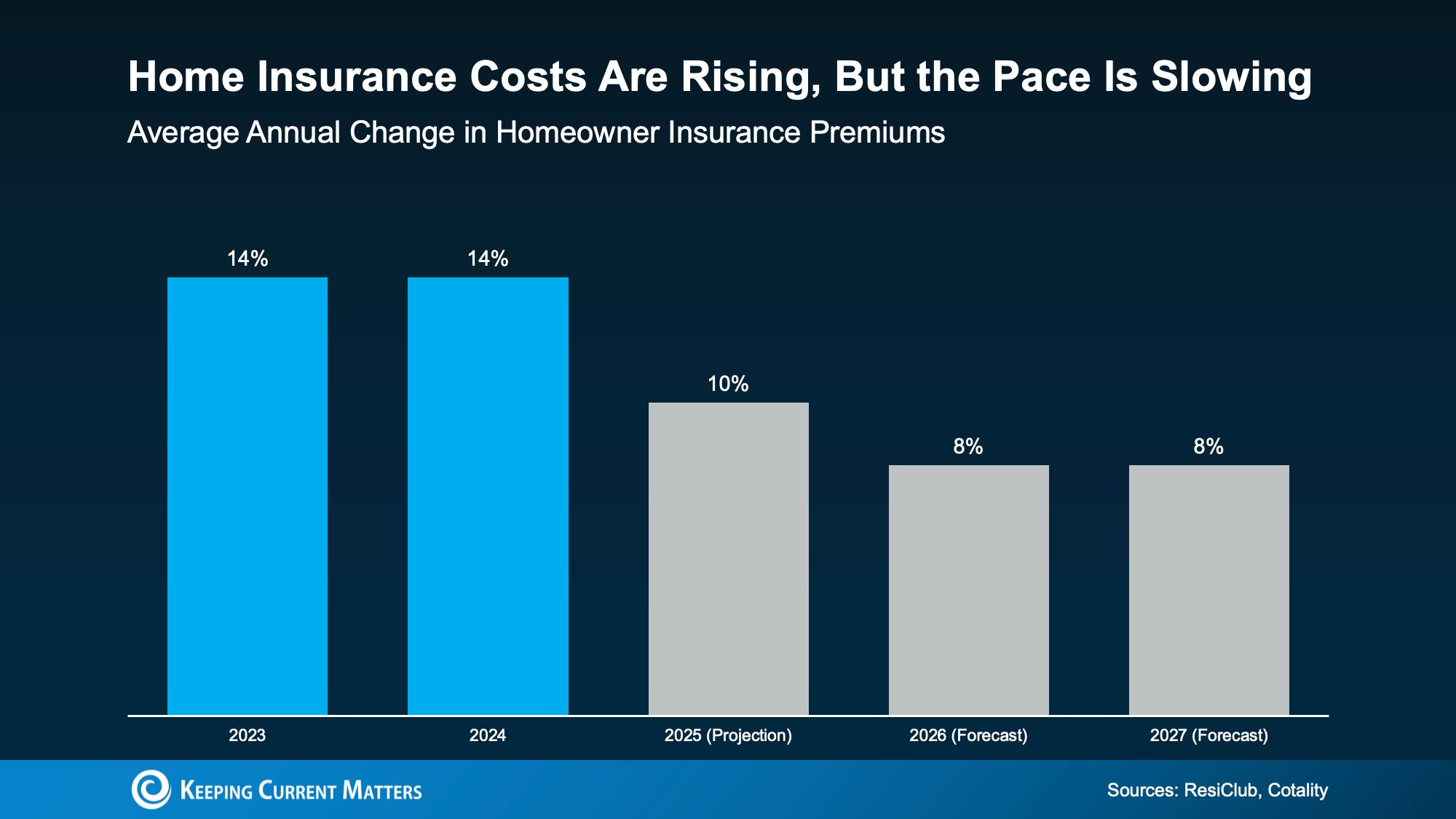

Taken together, these pressures are driving premiums higher. The chart below shows how insurance costs have climbed in recent years, with each bar representing the annual percentage increase. The encouraging news is that the pace of these increases may be starting to slow. According to ResiClub and Cotality, recent trends show:

- In 2023 and 2024, insurance costs rose by about 14% per year.

- In 2025, increases eased to roughly 10%.

- In 2026 and 2027, costs are projected to rise by about 8% annually.

Costs are still rising, but the rate of increase is beginning to slow—and there’s more good news ahead.

While insurance costs are climbing, mortgage rates have been trending downward—and that can help balance out some of the added expense. As Michael Gaines, Senior Vice President of Capital Markets at Cardinal Financial, explains:

“Higher taxes and insurance do add pressure, but they don’t wipe out the advantages of a lower interest rate. Even a modest rate drop—combined with the right loan program and thoughtful planning—can make homeownership more achievable. It’s not about one factor canceling out another. It’s about putting the right pieces together to create a workable solution.”

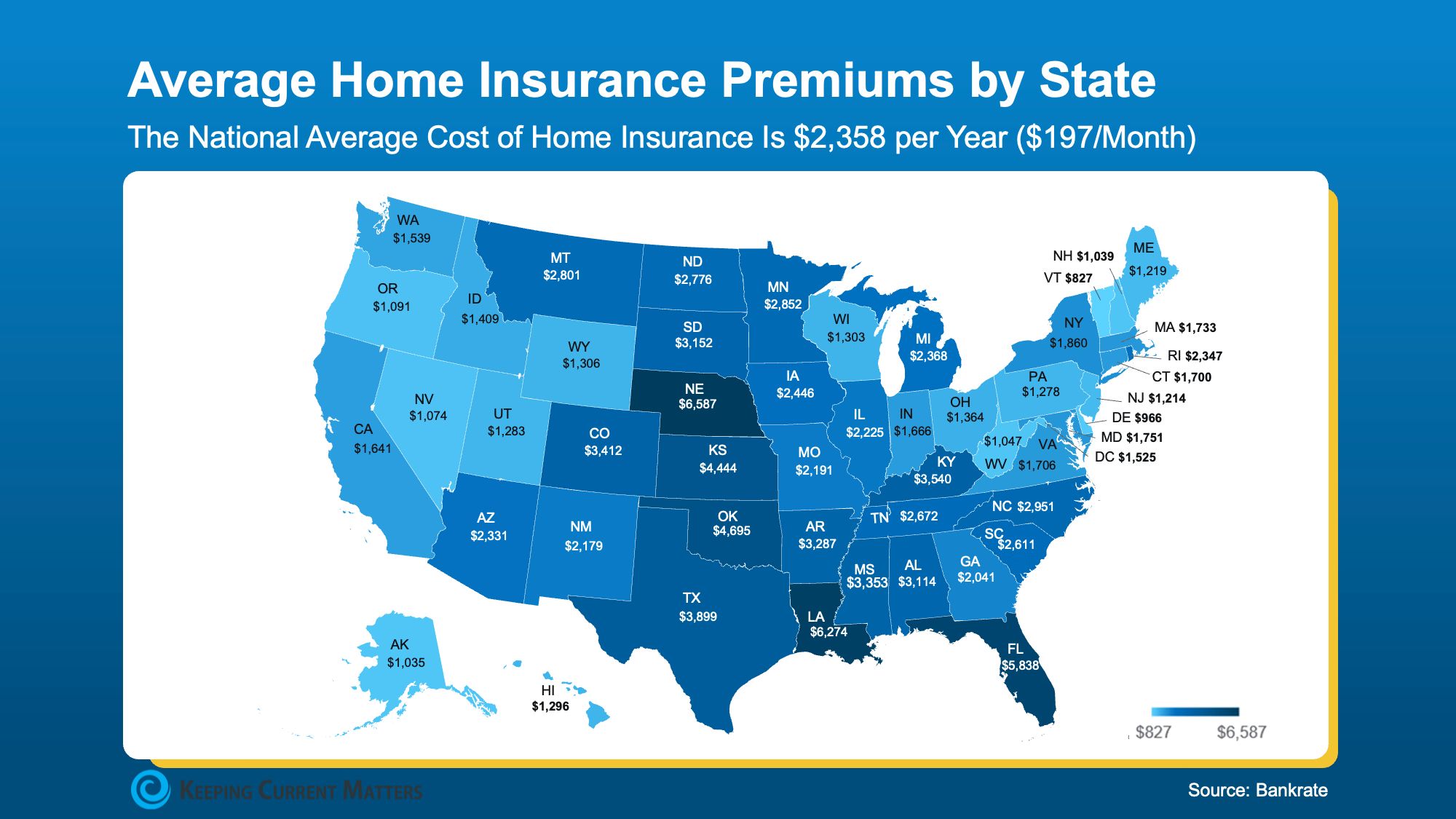

Insurance Costs Vary by Location

So, how much should you plan to budget? The answer depends on several factors—your home’s price, its location, the level of coverage you choose, and more. Like most things in real estate, insurance costs can vary widely from one area to another.

The map below offers a general snapshot of typical premiums by state, giving you a rough idea of what homeowners are paying in different parts of the country.

How Buyers Can Prepare for Rising Insurance Costs

In most cases, your first insurance payment is included in your closing costs. After that, it becomes an ongoing monthly expense. That’s why understanding rising premiums matters—it allows you to plan ahead, build them into your budget, and move forward with a clear picture of what you can realistically afford.

If you’re reviewing your budget and looking for ways to cut costs, Insurify and NerdWallet recommend these strategies to help secure the best possible rate:

- Shop Around – Get quotes from multiple providers to compare pricing.

- Bundle Policies – Combine your home and auto insurance to unlock discounts.

- Ask About Discounts – Make sure you’re taking advantage of any savings you qualify for.

- Highlight Upgrades – Improvements like a new roof or storm-resistant windows can lower premiums.

- Improve Your Credit – A higher credit score can lead to more favorable rates.

Bottom Line

If you’re planning to buy a home, make sure homeowner’s insurance is part of your financial strategy from day one. It’s not just another line item—it’s a core piece of protecting your investment and your long-term stability.

While premiums are rising, understanding what to expect, comparing options, and planning ahead can make a meaningful difference in how comfortably your purchase fits into your budget. With the right preparation, you can avoid surprises and feel confident about the numbers you’re committing to.

This is one area where cutting corners rarely pays off. The right coverage protects your home, your belongings, and your financial future—making it one of the smartest investments you’ll make alongside your property itself.

{ "@context": "https://schema.org", "@type": "FAQPage", "mainEntity": [ { "@type": "Question", "name": "Why is homeowners insurance so important when I buy a home?", "acceptedAnswer": { "@type": "Answer", "text": "Homeowners insurance is your financial safety net—it can help pay to repair or rebuild your home after covered events like fire, wind, or certain storms, replace covered personal belongings if they’re stolen or damaged, and provide liability protection if someone is hurt on your property and you’re found responsible." } }, { "@type": "Question", "name": "What does a standard homeowners insurance policy typically cover?", "acceptedAnswer": { "@type": "Answer", "text": "A standard policy generally includes coverage for the structure of your home (dwelling), other structures like fences or detached garages, personal property such as furniture and electronics, liability protection, guest medical payments, and additional living expenses if you can’t live in your home after a covered loss." } }, { "@type": "Question", "name": "Does homeowners insurance cover every type of disaster?", "acceptedAnswer": { "@type": "Answer", "text": "No. Standard policies commonly exclude floods and earthquakes, which often require separate policies or add-on coverage. Buyers should check local risks and confirm what’s covered (and what isn’t) with their insurer or agent." } }, { "@type": "Question", "name": "What is causing home insurance premiums to go up so much?", "acceptedAnswer": { "@type": "Answer", "text": "Premiums are rising largely because severe weather and natural disasters are becoming more frequent and costly, and because construction materials and labor have become more expensive—both of which increase the cost of insurance claims." } }, { "@type": "Question", "name": "How do higher construction costs affect what I pay for insurance?", "acceptedAnswer": { "@type": "Answer", "text": "When rebuilding a home costs more—due to higher prices for materials, labor, and permits—insurers raise premiums to keep up with larger potential payouts. Those increased claim costs are often passed on to homeowners through higher rates." } }, { "@type": "Question", "name": "Are natural disasters really making that big of a difference?", "acceptedAnswer": { "@type": "Answer", "text": "Yes. More frequent and severe events like wildfires, hail, hurricanes, and winter storms have increased both the number and cost of claims, especially in higher-risk areas, contributing to affordability challenges in many markets." } }, { "@type": "Question", "name": "How fast have home insurance costs been rising in recent years?", "acceptedAnswer": { "@type": "Answer", "text": "Industry data cited by ResiClub and Cotality indicates average U.S. homeowners premiums rose about 14% per year in both 2023 and 2024, reflecting a sharp increase over a short period." } }, { "@type": "Question", "name": "Are increases expected to continue at the same pace?", "acceptedAnswer": { "@type": "Answer", "text": "Not at the same pace. While premiums are still projected to rise, forecasts suggest the rate of increase may slow—about 10% in 2025 and roughly 8% annually in both 2026 and 2027." } }, { "@type": "Question", "name": "What does it mean when experts say the “rate of increase” is slowing?", "acceptedAnswer": { "@type": "Answer", "text": "It means prices are still rising, but not as quickly. For buyers, that suggests ongoing upward pressure on monthly housing costs, but potentially fewer large, sudden jumps than in the prior couple of years." } }, { "@type": "Question", "name": "How do rising insurance costs affect my overall housing budget?", "acceptedAnswer": { "@type": "Answer", "text": "Insurance is part of your total monthly housing payment. When premiums rise, your monthly payment can increase, which may affect how much home you can comfortably afford and how lenders view your overall housing expense." } }, { "@type": "Question", "name": "If insurance is going up, do lower mortgage rates still help me?", "acceptedAnswer": { "@type": "Answer", "text": "Yes. While higher taxes and insurance add pressure, a lower interest rate can reduce the mortgage portion of your payment enough to offset some of those increases—especially when paired with the right loan program and smart planning." } }, { "@type": "Question", "name": "Will lenders consider higher insurance costs when I apply for a mortgage?", "acceptedAnswer": { "@type": "Answer", "text": "Typically, yes. Lenders generally include estimated homeowners insurance (along with property taxes and principal and interest) when calculating your total monthly housing payment and determining how much you can borrow." } }, { "@type": "Question", "name": "Why do insurance costs vary so much by location?", "acceptedAnswer": { "@type": "Answer", "text": "Premiums depend heavily on local risk and costs—such as exposure to wildfires, hurricanes, hail, and winter storms, as well as crime rates and local rebuilding expenses—so similar homes in different areas can have very different insurance bills." } }, { "@type": "Question", "name": "Are some states facing more serious insurance challenges than others?", "acceptedAnswer": { "@type": "Answer", "text": "Yes. Some high-risk states have faced affordability and availability problems as insurers raise rates, tighten underwriting standards, or reduce exposure in certain regions." } }, { "@type": "Question", "name": "How can I get a rough idea of what premiums look like where I’m buying?", "acceptedAnswer": { "@type": "Answer", "text": "Start with state-by-state premium snapshots from reputable consumer and research sources, then request quotes from insurers or local brokers for the specific property type and neighborhood you’re considering." } }, { "@type": "Question", "name": "When will I first pay for homeowners insurance as a buyer?", "acceptedAnswer": { "@type": "Answer", "text": "Many buyers pay the first year of homeowners insurance at closing—either directly or through an escrow account. After closing, ongoing premiums are often collected monthly as part of the mortgage payment (if you escrow)." } }, { "@type": "Question", "name": "How should I factor insurance into my homebuying budget?", "acceptedAnswer": { "@type": "Answer", "text": "Treat insurance as a core line item: get quotes early during your search, include the premium in your monthly affordability calculations, and stress-test your budget for possible future increases." } }, { "@type": "Question", "name": "Could under-insuring my home help me save money safely?", "acceptedAnswer": { "@type": "Answer", "text": "Under-insuring may reduce premiums short term, but it can leave you without enough coverage to rebuild or replace belongings after a major loss—turning a manageable problem into a serious financial hardship." } }, { "@type": "Question", "name": "What are some practical ways to lower my homeowners insurance premium?", "acceptedAnswer": { "@type": "Answer", "text": "Common strategies include shopping multiple quotes, bundling home and auto policies, raising your deductible if it fits your risk tolerance, asking about available discounts, and improving safety features like smoke detectors or security systems." } }, { "@type": "Question", "name": "How does bundling policies help me save?", "acceptedAnswer": { "@type": "Answer", "text": "Many insurers offer multi-policy discounts when you bundle home and auto (and sometimes other coverage), which can lower the combined cost compared with purchasing policies separately." } }, { "@type": "Question", "name": "What types of discounts should I ask about?", "acceptedAnswer": { "@type": "Answer", "text": "Discounts can include savings for being claim-free, installing monitored security systems, having a newer roof, adding safety features, or maintaining a strong credit profile in states where credit-based insurance scoring is used." } }, { "@type": "Question", "name": "Can home upgrades really reduce my premium?", "acceptedAnswer": { "@type": "Answer", "text": "Yes. Risk-reducing upgrades—like a new roof, storm-rated windows, wildfire-resistant materials, or defensible space improvements—may lower risk and can qualify you for discounts or mitigation credits with some insurers." } }, { "@type": "Question", "name": "How important is my credit score for insurance costs?", "acceptedAnswer": { "@type": "Answer", "text": "In many states, insurers use credit-based insurance scores as part of pricing, and higher scores are often associated with lower premiums. However, rules vary by state, and some states restrict or prohibit this practice." } }, { "@type": "Question", "name": "Should I switch insurers if my rate jumps?", "acceptedAnswer": { "@type": "Answer", "text": "If your premium increases sharply, gather competing quotes and compare coverage details. You may find a better rate for similar protection, but also consider claims service and overall reputation before switching." } }, { "@type": "Question", "name": "How much dwelling coverage should I choose?", "acceptedAnswer": { "@type": "Answer", "text": "You generally want enough dwelling coverage to rebuild your home at today’s construction costs. That amount can differ from your purchase price or tax assessment, so use the insurer’s replacement-cost estimator or guidance from your agent." } }, { "@type": "Question", "name": "Do I need replacement cost or actual cash value for my belongings?", "acceptedAnswer": { "@type": "Answer", "text": "Replacement cost coverage pays what it takes to buy new items of similar kind and quality, while actual cash value subtracts depreciation. Many buyers prefer replacement cost to reduce out-of-pocket expenses after a loss." } }, { "@type": "Question", "name": "What is liability coverage and how much do I need?", "acceptedAnswer": { "@type": "Answer", "text": "Liability coverage helps pay legal and medical costs if you’re found responsible for injuries or damage to others. Many homeowners choose limits above the default minimums to better protect assets from lawsuits." } }, { "@type": "Question", "name": "Should I consider an umbrella policy on top of homeowners insurance?", "acceptedAnswer": { "@type": "Answer", "text": "If you have significant assets or income to protect, an umbrella policy can add extra liability coverage above your home and auto limits, often at a relatively modest cost per additional dollar of protection." } }, { "@type": "Question", "name": "What if insurers are pulling out of my area or limiting coverage?", "acceptedAnswer": { "@type": "Answer", "text": "In higher-risk regions, buyers may need specialized brokers, state-backed “last resort” programs, or surplus-lines carriers. Expect stricter requirements, higher premiums, and more detailed underwriting." } }, { "@type": "Question", "name": "How can I feel confident moving forward despite rising insurance costs?", "acceptedAnswer": { "@type": "Answer", "text": "Get multiple quotes early, understand local risks, match coverage to true replacement and liability needs, and plan for future premium increases alongside your mortgage and tax projections. A realistic budget and strong coverage help protect both your home and long-term financial stability." } } ] }

Categories

Recent Posts

GET MORE INFORMATION