Rent vs. Buy: What the Real Numbers Say

Renting can seem like the simpler path. No large upfront investment. No unexpected repair bills. No long-term obligation tying you down.

But then the rent increases. And it increases again. What once felt flexible starts to feel costly — especially when none of that payment builds ownership. Over time, that cycle can feel hard to break.

There’s a lot of noise right now about homeownership being out of reach. Yet when you actually run the numbers, today’s reality may look more balanced than the headlines suggest.

In Many Markets, Buying Costs Less Than Renting

In many markets right now, the monthly cost to own a home is lower than renting a three-bedroom property. Recent data from ATTOM shows that’s the case in nearly 58% of counties nationwide (see chart below).

And that comparison already includes expenses like homeowners insurance and standard maintenance costs.

Put simply, while it may not seem that way at first glance, the data shows rent frequently puts more pressure on a monthly budget than owning. That shift is being driven by moderating home price growth, rising inventory levels, and mortgage payments beginning to soften as interest rates trend downward.

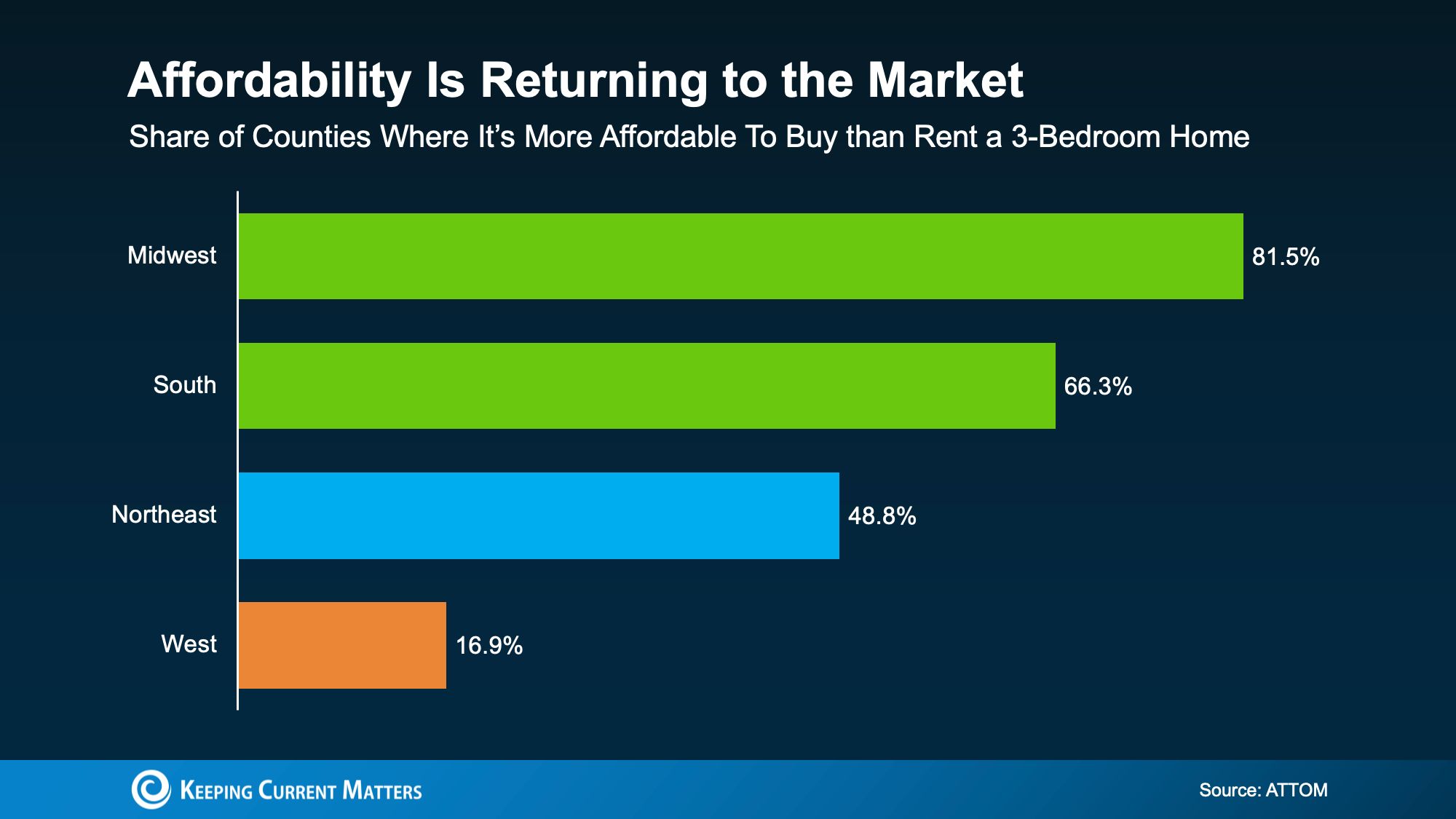

Market Conditions Vary Across Regions

While the national trend has tilted in favor of buying, that doesn’t mean it’s the better financial move in every market — or for every renter.

Although owning is more affordable than renting in nearly 58% of counties across the country, that percentage varies significantly by region (see graph below):

The most noticeable gains are showing up in the Midwest and the South, while affordability in many Western markets remains more constrained.

Bottom line: affordability is highly location-specific. The only way to understand how the rent-versus-buy equation works in your area is to analyze the local data.

What’s Preventing Buyers From Making a Move?

You might be following along and thinking, “That all sounds good — but the upfront costs still feel out of reach.” If so, you’re not alone.

For many renters, the real obstacle isn’t just the monthly payment. It’s coming up with the down payment in the first place.

You’re not without solutions. What often gets overlooked is that there are thousands of down payment assistance programs nationwide — and many eligible buyers don’t even realize they qualify.

On average, these programs provide about $18,000 in support.

That level of assistance can offset a meaningful portion of your down payment or closing costs — reducing how much cash you actually need upfront.

Pair that with monthly payments that may be more manageable than expected, particularly as rates ease and price growth moderates, and homeownership can start to look much more attainable than it first appears.

Bottom Line

This isn’t about telling everyone to run out and buy tomorrow.

It’s about recognizing that renting isn’t automatically the cheaper or safer choice — and that ownership may be more achievable than it seems when you step back and evaluate the full financial picture.

If you’re renting and caught in the “maybe someday” mindset, a quick conversation with a local real estate professional or lender could bring clarity. No pressure — just a realistic look at your options and whether making a move makes sense for you right now.

{ "@context": "https://schema.org", "@type": "FAQPage", "mainEntity": [ { "@type": "Question", "name": "In what percentage of counties nationwide is buying a home currently more affordable than renting?", "acceptedAnswer": { "@type": "Answer", "text": "According to recent data from ATTOM, buying is more affordable than renting in nearly 58% of counties across the country. That comparison already factors in expenses like homeowners insurance and standard maintenance costs — not just the mortgage payment itself." } }, { "@type": "Question", "name": "What factors are driving the shift toward buying being more cost-effective than renting?", "acceptedAnswer": { "@type": "Answer", "text": "Three main forces are behind the trend: moderating home price growth, rising inventory levels, and mortgage payments beginning to soften as interest rates trend downward. Together, these are making ownership more competitive with renting on a monthly basis in many markets." } }, { "@type": "Question", "name": "Does the national trend toward buying mean homeownership makes financial sense everywhere?", "acceptedAnswer": { "@type": "Answer", "text": "No. While buying is more affordable than renting in nearly 58% of counties nationally, the picture varies significantly by region. The Midwest and South are seeing the most noticeable gains in affordability, while many Western markets remain more constrained. Affordability is highly location-specific, so analyzing local data is essential before drawing conclusions." } }, { "@type": "Question", "name": "What is the biggest obstacle preventing renters from transitioning to homeownership?", "acceptedAnswer": { "@type": "Answer", "text": "For many renters, the challenge isn't the monthly mortgage payment — it's the upfront down payment. Coming up with that initial cash can feel like an insurmountable barrier, even when ongoing ownership costs may actually be lower than their current rent." } }, { "@type": "Question", "name": "Are there programs that can help with down payment costs, and how much assistance do they typically provide?", "acceptedAnswer": { "@type": "Answer", "text": "Yes. There are thousands of down payment assistance programs available nationwide, and many eligible buyers are unaware they qualify. On average, these programs provide around $18,000 in support, which can meaningfully offset a down payment or closing costs and reduce the amount of cash a buyer needs upfront." } }, { "@type": "Question", "name": "What is the core takeaway from comparing rent vs. buy costs?", "acceptedAnswer": { "@type": "Answer", "text": "Renting is not automatically the cheaper or safer financial choice. When you factor in rising rents, the absence of equity building, available assistance programs, and moderating ownership costs, homeownership can be more attainable than it appears on the surface. The recommendation is to review the full financial picture — ideally with a local real estate professional or lender — before assuming ownership is out of reach." } } ] }

Categories

Recent Posts

GET MORE INFORMATION