How Rising Inflation Could Impact Your Home Move

New inflation data is raising questions about where mortgage rates and home prices could be headed next. Here’s what the numbers are telling us, why it matters for the housing market, and what it means if you're planning to buy or sell.

Inflation Is Rising: What It Really Means

The government uses several measures to track inflation, and one of the most closely watched is the Personal Consumption Expenditures (PCE) Price Index. This report looks at how the cost of everyday goods and services has changed compared to a year ago. If your grocery, utility, or fuel bills feel higher lately, you're already seeing the effects firsthand.

PCE has been getting a lot of attention recently because it has started moving higher again. As shown by the yellow line on the chart below, inflation has accelerated since February. One of the primary factors behind this increase has been rising energy costs, driven in part by ongoing tensions in the Middle East that have put upward pressure on oil, gas, and transportation prices.

You may have noticed a second line on the chart. The blue line represents Core PCE, which measures inflation while excluding food and energy costs. The Federal Reserve pays particularly close attention to this figure because energy prices can fluctuate significantly from month to month, sometimes creating a distorted picture of broader inflation trends.

There is some encouraging news in the data.

While Core PCE has been moving higher, it hasn't increased nearly as quickly as the overall inflation measure. That suggests much of the recent rise in inflation is being driven by energy-related costs and global events rather than broad-based price increases across the economy. If those external pressures begin to ease, inflation could moderate as well.

Why Inflation Trends Matter for Mortgage Rates

Here's where it connects to the housing market. When inflation remains elevated, the Federal Reserve often keeps interest rates higher for longer—or may even raise them further—in an effort to slow spending and bring inflation under control. While mortgage rates don't move in lockstep with the Federal Funds Rate, Fed policy plays an important role in shaping the overall interest rate environment.

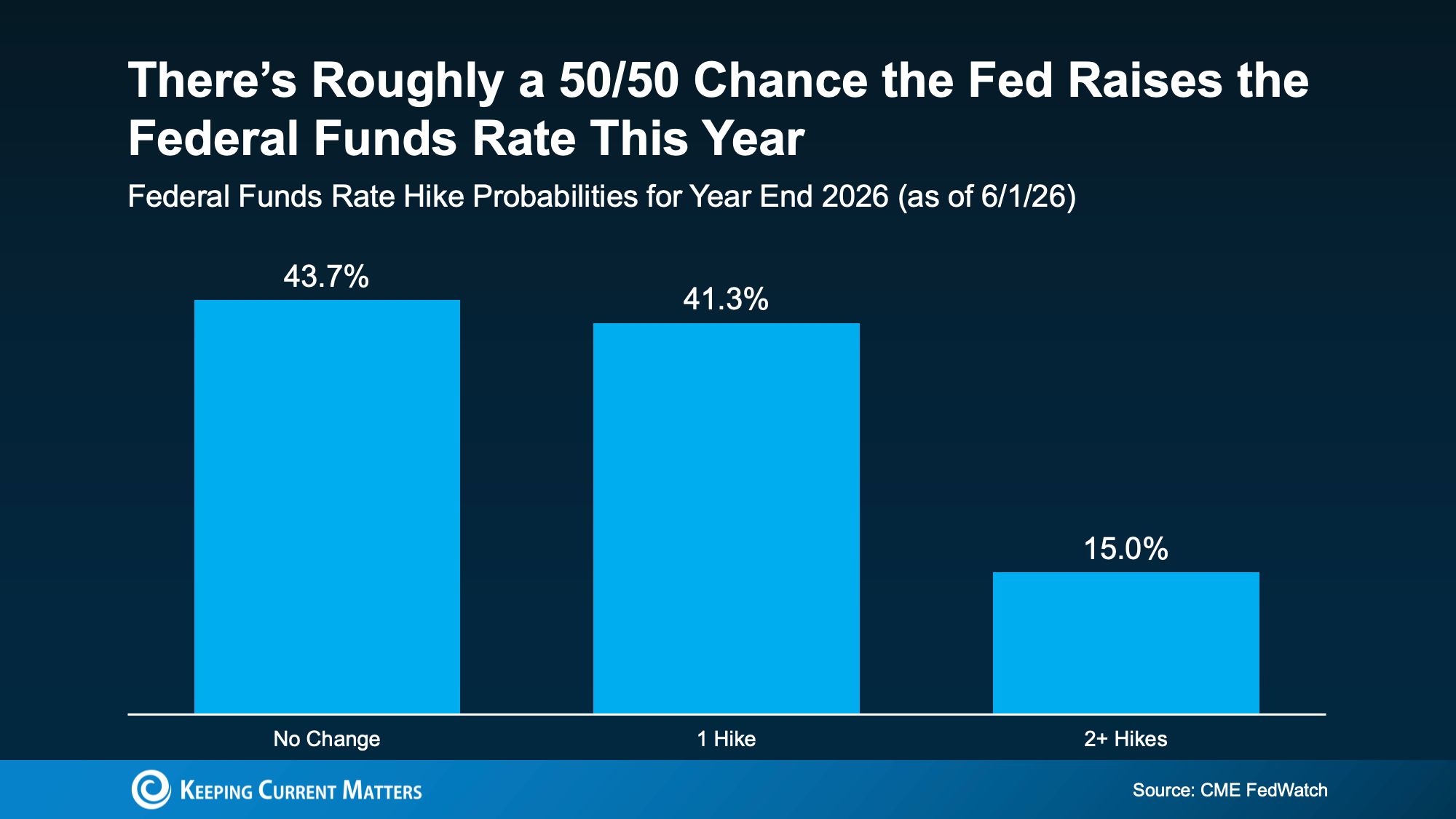

Based on current market expectations, there's roughly a 50% chance the Federal Reserve could raise rates again before the end of 2026, according to CME FedWatch. That uncertainty is one reason mortgage rates have remained higher than many buyers were hoping for (see graph below).

While it's still too early to know exactly how this will play out, the latest inflation data suggests mortgage rates may remain elevated for longer than many had anticipated. A rate hike isn't a certainty, but expectations for significant rate relief in the near term have become less likely.

If you've been holding off on buying or selling in hopes that mortgage rates will fall substantially, this latest inflation report is a reminder that rates could remain elevated for some time. While no one can predict the future with certainty, the direction of rates will largely depend on how inflation, economic growth, and global events unfold in the months ahead.

As financial analysts continue to point out, energy prices and bond yields have eased slightly from recent highs, but they remain well above where they were earlier this year. Until some of the geopolitical uncertainty is resolved, inflationary pressures and borrowing costs are likely to stay higher than many consumers would prefer.

Why Today's Housing Market Is Nothing Like 2008

It's important to separate economic uncertainty from the idea of a housing crash. While today's market has its challenges, the factors that fueled the 2008 housing crisis simply aren't present on the same scale. Here's what makes today's market different:

- Housing inventory remains relatively limited, with supply still below historical norms in many markets.

- Most homeowners have built substantial equity, providing a strong financial cushion.

- Mortgage lending standards are significantly stricter, resulting in more qualified borrowers.

- The biggest obstacle facing the market today is affordability driven by higher prices and interest rates—not a surge of distressed homeowners forced to sell.

A challenging market doesn't necessarily mean an unhealthy one. Conditions may feel difficult right now, but there's a significant difference between a market facing headwinds and one that is in decline.

What Buyers and Sellers Can Do Right Now

Higher mortgage rates don't mean homeownership is off the table. They simply require a different approach than buyers may have used in the past. The good news is that there are several strategies available, and the right one depends on your goals, finances, and timeline:

- Talk with your lender about financing strategies that may improve affordability. Options such as adjustable-rate mortgages (ARMs), temporary rate buydowns, or other loan programs could help reduce monthly payments, especially in the early years of homeownership.

- Take advantage of available resources, including first-time homebuyer programs, down payment assistance, grants, and seller concessions that may help lower your upfront or ongoing costs.

- Maintain regular communication with a knowledgeable real estate agent and lender. Market conditions can change quickly, and being prepared puts you in a stronger position to act when opportunities arise.

A well-thought-out plan that aligns with your goals is often far more valuable than waiting for the "perfect" market conditions, which may never arrive.

Bottom Line

Higher inflation is likely to keep pressure on mortgage rates for the time being, but that doesn't mean your real estate goals need to be put on hold. The key isn't waiting for the perfect market—it's understanding your options and making informed decisions based on your unique circumstances.

Have questions about buying, selling, or refinancing? Reach out to a local real estate professional or lender to discuss the best path forward.

Categories

Recent Posts

GET MORE INFORMATION