Record-High Mortgage Debt Sounds Alarming, But Here’s the Context Headlines Miss

You may have seen the recent headlines about mortgage debt in America reaching an all-time high. Maybe your brother-in-law even brought it up at dinner like he’d been saving it all week for a heated debate.

And to be fair, he’s not entirely wrong. Mortgage debt has hit a record high. But that’s only part of the story and the part missing from most headlines completely changes the bigger picture.

Homeowners are in a much stronger position than the headlines make it seem, and today’s housing market has more stability than most people realize.

The Headline Number Is Real, But It Doesn’t Tell the Full Story

Yes, according to the Federal Reserve, mortgage debt in the U.S. is now around $14 trillion, the highest level on record. And when that number shows up next to stories about households feeling stretched, it’s easy to jump to a scary conclusion.

But the data tells a more complete story:

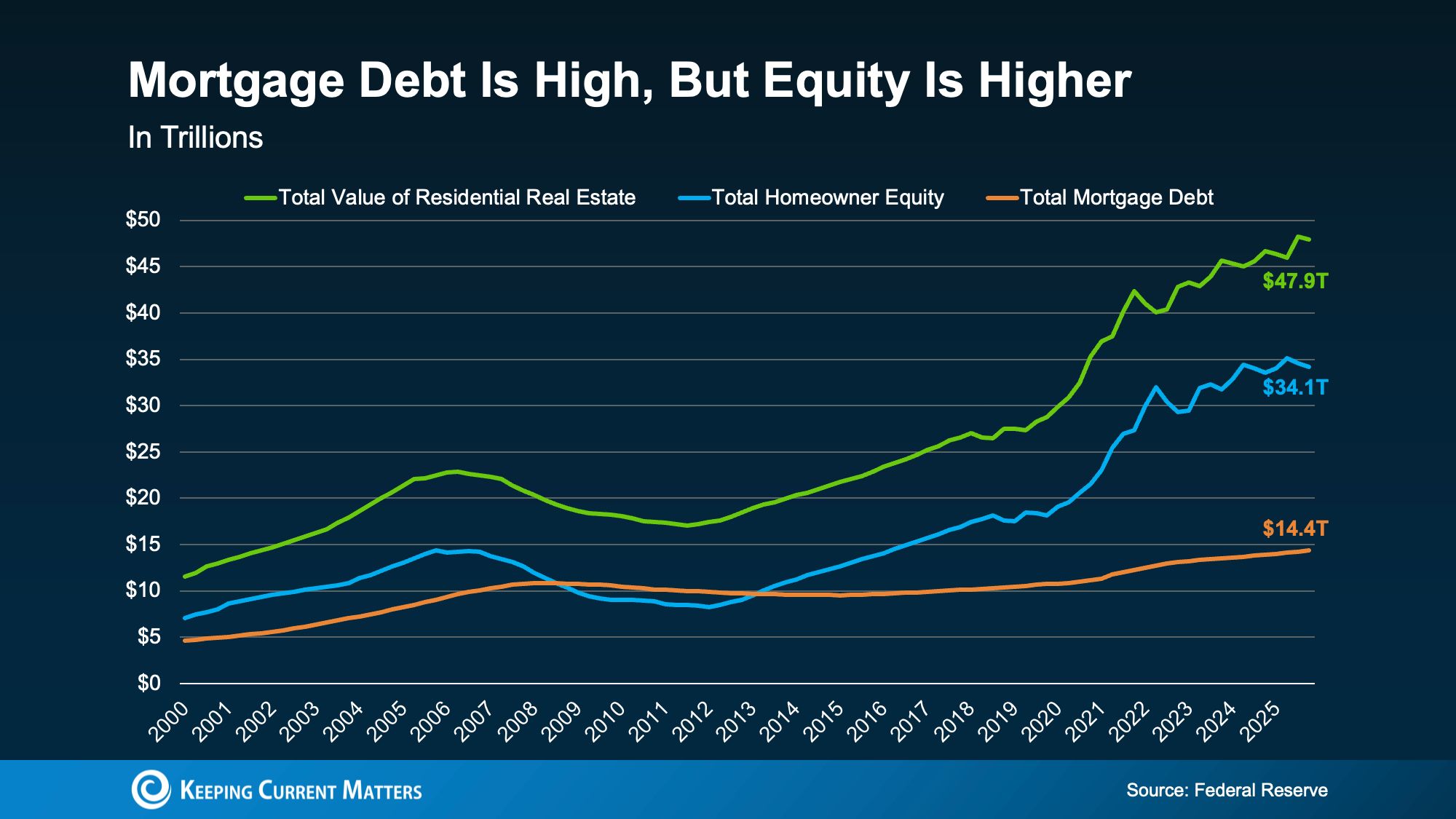

This chart from the Federal Reserve compares three key housing trends from 2000 through today: the total value of all homes in the U.S. (green line), the amount of equity homeowners have built (blue line), and the total mortgage debt tied to those homes (orange line).

Today, U.S. home values are estimated at roughly $47.9 trillion. Homeowners currently hold about $34.1 trillion in equity. And the mortgage debt making headlines? That stands at approximately $14.4 trillion.

Yes, mortgage debt is at a record high. But homeowner equity is more than twice that amount and is also sitting near record levels.

And that’s the part most headlines leave out. Look back at the period between 2008 and 2013, when the orange line climbed above the blue line. That’s when the housing market was facing real stress. During that time, many homeowners owed more than their homes were worth, leaving little to no financial cushion.

When home prices fell in 2008, millions of homeowners suddenly owed more on their mortgages than their homes were worth. That’s what a real housing crisis looks like — people had little to no equity cushion to protect them. That’s not the situation today. In fact, it’s the complete opposite.

The gap between what homeowners owe and what they own is historically strong. Today’s homeowners hold substantially more equity than debt, giving them a much healthier financial position than during the last housing crash.

Most Homeowners Are Standing on Solid Ground

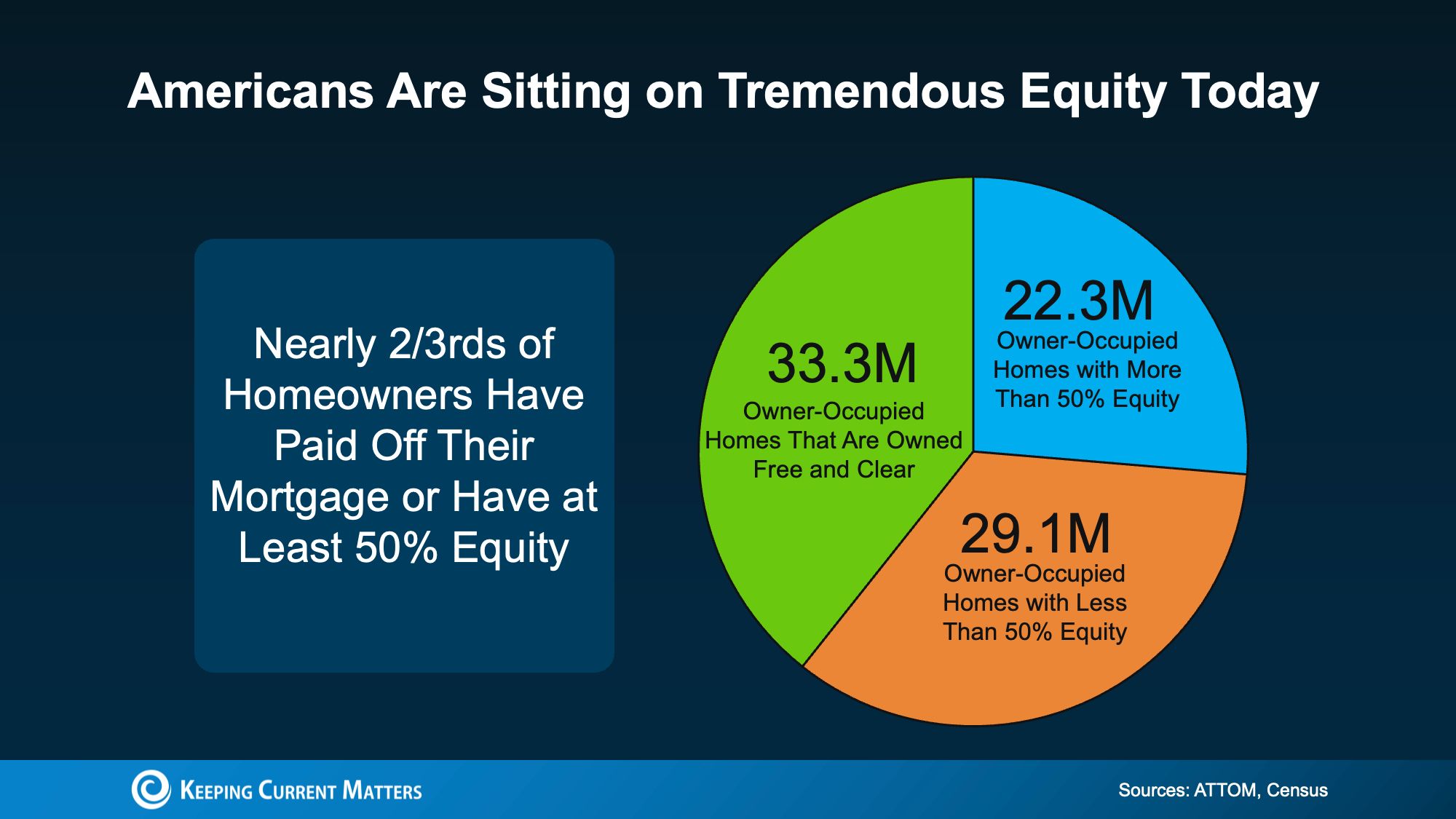

Nationally, homeowner equity is strong. But what does that mean for the average homeowner? This next chart uses data from ATTOM and the Census to show what that looks like on a more personal level:

Of all owner-occupied homes in the U.S., 33.3 million are owned free and clear — no mortgage, no lender, and no foreclosure risk tied to a mortgage payment. Another 22.3 million homeowners have more than 50% equity in their homes.

Put those together, and nearly two-thirds of homeowners have either paid off their home completely or built enough equity to be in a very strong financial position.

The remaining group — 29.1 million homes with less than 50% equity — doesn’t automatically signal trouble. Many of those homeowners bought more recently, are steadily building equity, and are still in a healthy position.

The takeaway: this is not a housing market hanging by a thread. It’s one supported by an unusually strong equity foundation.

Bottom Line

The headlines about record-high mortgage debt can sound alarming, but without the full context, they don’t tell the real story.

Homeowner equity remains near historic highs, property values have grown significantly over time, and most homeowners today are in a far stronger financial position than they were leading into the 2008 crash. The underlying conditions that fueled that housing crisis simply aren’t present in today’s market.

If you’re trying to understand what today’s market means for you — whether you’re considering buying, selling, investing, or just keeping an eye on things — talking with a knowledgeable local real estate professional can help bring clarity to the numbers and the noise. Reach out anytime with questions.

```json { "@context": "https://schema.org", "@type": "FAQPage", "mainEntity": [ { "@type": "Question", "name": "What is the current total U.S. mortgage debt, and why does it sound alarming?", "acceptedAnswer": { "@type": "Answer", "text": "Mortgage debt has reached approximately $14.4 trillion, an all-time record. It sounds alarming because headlines often present this number without the broader context of home values and homeowner equity." } }, { "@type": "Question", "name": "What is the total value of U.S. homes today, and how much equity do homeowners hold?", "acceptedAnswer": { "@type": "Answer", "text": "U.S. home values are estimated at roughly $47.9 trillion, with homeowners holding about $34.1 trillion in equity, which is more than twice the total mortgage debt." } }, { "@type": "Question", "name": "What made the 2008–2013 housing crisis so dangerous compared to today?", "acceptedAnswer": { "@type": "Answer", "text": "During that period, mortgage debt exceeded homeowner equity, meaning millions of homeowners owed more than their homes were worth and had no financial cushion when prices fell. Today, the situation is the opposite." } }, { "@type": "Question", "name": "How many homeowners own their homes free and clear?", "acceptedAnswer": { "@type": "Answer", "text": "Approximately 33.3 million owner-occupied homes have no mortgage at all." } }, { "@type": "Question", "name": "How many homeowners have more than 50% equity in their homes?", "acceptedAnswer": { "@type": "Answer", "text": "Another 22.3 million homeowners have built more than 50% equity in their homes." } }, { "@type": "Question", "name": "What portion of homeowners are considered to be in a strong financial position?", "acceptedAnswer": { "@type": "Answer", "text": "Nearly two-thirds of all homeowners are considered to be in a strong financial position because they either own their home outright or hold more than 50% equity." } }, { "@type": "Question", "name": "Does having less than 50% equity mean a homeowner is in trouble?", "acceptedAnswer": { "@type": "Answer", "text": "Not necessarily. Many homeowners in that group bought recently, are steadily building equity over time, and remain in a healthy financial position." } }, { "@type": "Question", "name": "What is the key takeaway about today's housing market?", "acceptedAnswer": { "@type": "Answer", "text": "Despite record mortgage debt, today's housing market is supported by historically strong equity levels, rising property values, and a far more stable foundation than existed before the 2008 crash." } } ] } ```

Categories

Recent Posts

GET MORE INFORMATION