Understanding Coverage: Home Warranty vs. Homeowners Insurance

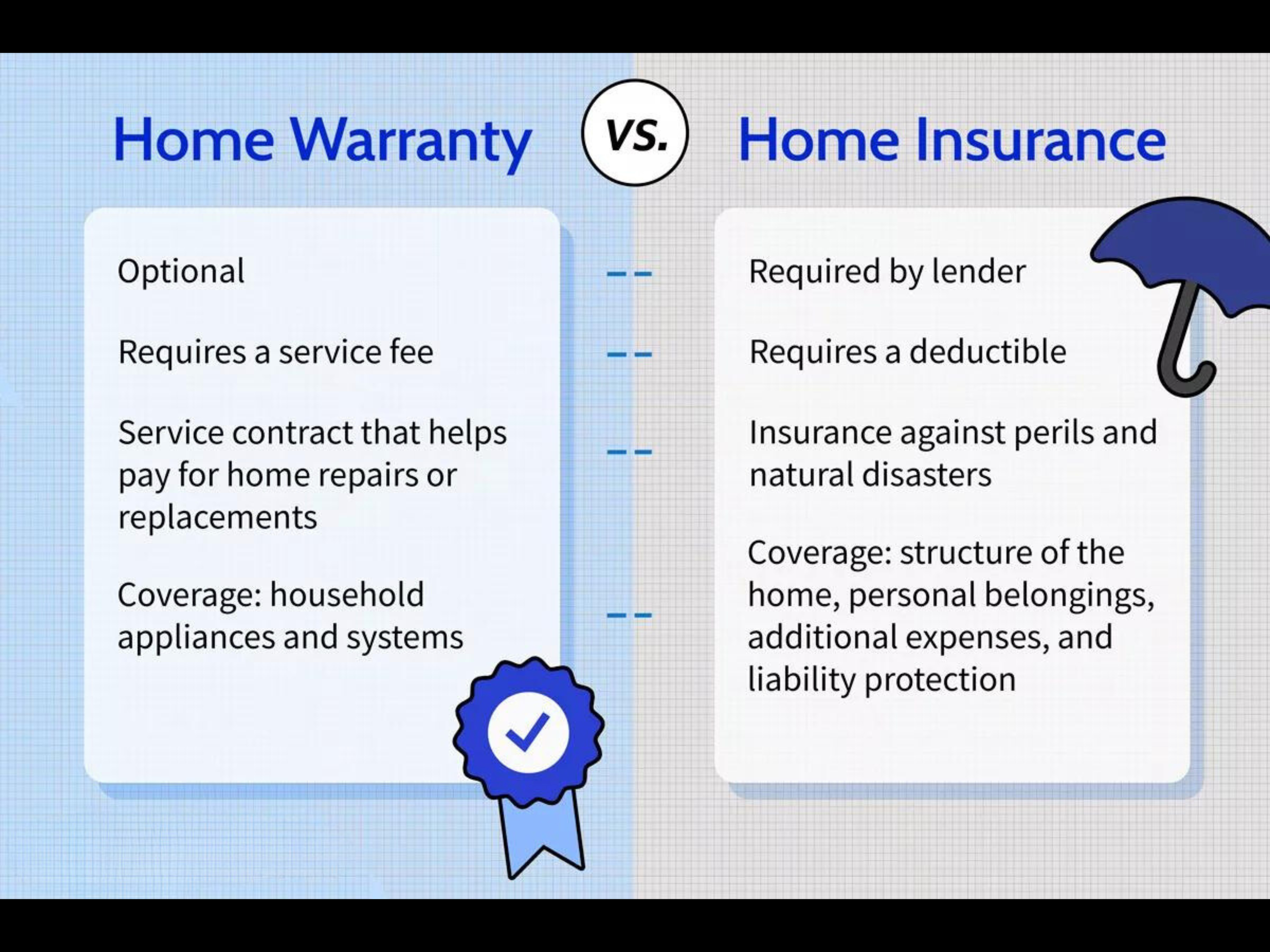

A home warranty includes the service and repair or replacement of your home's major systems and appliances for typically a one-year period. This type of warranty is provided by a home warranty company and differs from homeowners insurance, which offers financial protection in the event of a disaster or accident. Standard homeowners insurance policies cover a home's structure and possessions in case of specified perils such as weather events, fires, or floods.

Home warranties and homeowners insurance policies are both valuable tools for reducing the risk and potential financial burden of homeownership. However, it is important to understand the differences between them. A home warranty covers the service, repair, or replacement of home systems and appliances, while homeowners insurance provides financial protection in the event of a disaster or accident.

Is a Home Warranty Similar to Homeowners Insurance?

A home warranty should not be seen as a substitute for homeowners insurance.

A home warranty plan provides coverage for the service, repair, and replacement of essential home systems such as HVAC, electrical, and plumbing, as well as major appliances like refrigerators and dishwashers. The specifics of what is covered are detailed in the contract, with some plans offering more comprehensive coverage than others.

Conversely, homeowners insurance protects against damage or loss resulting from specific risks, including wind, hail, fire, vandalism, or theft. More inclusive homeowners insurance policies, known as “all risk,” cover a broader range of perils with fewer exclusions.

Regardless of whether you opt for a basic policy covering named perils or a more extensive all-risk policy, investing in homeowners insurance is essential for any homeowner. It's often a requirement by mortgage or home equity lenders, highlighting a significant distinction between home insurance and home warranties.

While not mandatory, a home warranty can complement homeowners insurance by covering damages not typically included in home insurance policies. By addressing some of the exclusions found in homeowners insurance, a home warranty plan adds an extra layer of coverage, mitigating the financial risks associated with homeownership.

Although home warranties are not as critical as homeowners insurance, they offer additional protection that can ease the financial strain of unforeseen repairs and replacements of systems and appliances.

What Does a Home Warranty Include?

The systems and appliances in your home have a limited lifespan. When a system or appliance malfunctions or stops working due to normal wear and tear, the cost of repair or replacement can be an unforeseen financial burden. A home warranty mitigates this risk by providing service, repair, or replacement for major built-in household appliances and systems.

Home warranties typically cover a range of appliances and major systems, which can include:

Appliances

- Dishwashers

- Ovens

- Refrigerators (often excluding the ice maker)

Systems

- HVAC

- Plumbing

- Electrical

Additionally, some companies offer "cafeteria plan" home warranties that allow coverage for specific items chosen by the homeowner. It's important to note that home warranties do not cover cosmetic defects, such as scratches on stainless steel appliances.

When purchasing a home warranty, it's essential to carefully review the contract to ensure that the systems and appliances you are concerned about are listed as covered assets. Certain parts of these items, such as a refrigerator's beverage dispenser and water line, may be excluded from coverage.

What is Covered Under Homeowners Insurance?

The coverage provided by homeowners insurance varies depending on the type of policy. A named-peril policy offers basic protection against events such as fire, wind, hail, theft, or vandalism. On the other hand, an all-risk homeowners insurance policy provides broader coverage with fewer exclusions, typically requiring a higher premium.

Typical home insurance coverage includes:

- Damage to property and liability for injuries to guests on your property

- Damage caused by natural disasters, with some exceptions (standard exclusions being flooding, earthquakes, wear and tear, and vermin damage)

- Damage to the home structure

- Damage to personal belongings

- Personal liability

- Additional living expenses if the home is uninhabitable due to a named peril (e.g., fire or wind)

It's important to note that homeowners insurance doesn't cover all perils, such as floods and earthquakes, and may require specialized insurance for such events. Additionally, coverage levels and exclusions can vary between policies, so it's essential to review the details before making a purchase.

Who Should Consider Purchasing a Home Warranty?

Ideal for:

✓ Individuals with aging appliances or HVAC systems

✓ Those who prefer not to source their own service technicians

✓ Individuals seeking to mitigate the risk of significant unexpected expenses

Not recommended for:

✗ Individuals with predominantly new appliances still under their manufacturers' warranties

✗ Those looking to avoid the risk of exclusions and limitations

✗ Individuals who prefer to engage their own service professionals

A home warranty typically entails a one-year service contract with a warranty company, covering the service, repair, and replacement of major home systems and appliances. Homeowners may find a home warranty beneficial as it is designed to reduce the risk of unforeseen expenses.

Consider a home warranty if you have an aging HVAC system, as the cost of replacement can be substantial, and a home warranty can alleviate the financial burden if the system malfunctions. It is also advantageous for covering aging appliances, particularly if the manufacturers' warranties have expired.

If you lack a reliable network of home service professionals for plumbing, electrical, or appliance repairs, a home warranty can be advantageous. Upon filing a claim with the home warranty company, a local technician will be dispatched if the issue is covered.

However, it's important to note that a home warranty differs from home insurance. When contemplating the purchase of a home warranty, attention should be paid to the specifics and fine print.

Home warranties may not be worthwhile if your appliances are new and still under their original manufacturer's warranties, or if you have obtained an extended warranty. Furthermore, warranties often exclude external contractors.

Who Should Consider Purchasing Homeowners Insurance?

Ideal for:

✓ Individuals obtaining a loan for a home purchase

✓ Those prioritizing financial security

✓ Homeowners seeking to protect their property

Not Recommended for:

✗ Individuals unwilling or unable to afford an extra expense

✗ Those solely seeking coverage for normal wear and tear

It's advisable for every homeowner to procure homeowners insurance, and for renters, purchasing renters insurance is essential. While homeowners insurance isn't mandated by law, lenders typically mandate its purchase. This requirement stems from the fact that, just as your home is a significant asset for you, it represents a substantial investment for your mortgage lender.

In the event of a fire, adverse weather conditions, theft, or vandalism, the consequences are shared by all parties. Without homeowners insurance, you'd be responsible for covering the costs. Even if you own your home outright, homeowners insurance remains crucial to protect against total loss scenarios that could otherwise render rebuilding financially unfeasible.

It's important to note that a home warranty does not serve as a substitute for homeowners insurance. While you may opt to purchase a home warranty or forgo the additional coverage altogether, homeowners insurance remains essential for safeguarding your residence against unforeseen circumstances.

Furthermore, if you find any ambiguity in your coverage, it's advisable to seek clarification from your insurance or warranty provider and ensure that all necessary details are documented in writing.

Categories

Recent Posts

GET MORE INFORMATION