The Housing Market Isn't as Weak as the Headlines Suggest

You've probably seen plenty of headlines suggesting the housing market is struggling, higher mortgage rates, affordability challenges, and predictions of a slowdown. But the data tells a different story. Today's market isn't 2020 or 2021, and it was never expected to be. Those years were an anomaly,

The One Factor Driving Today’s Home Prices

You've probably heard that home prices are starting to cool—and that's true at the national level. But when you take a closer look at local markets, the story becomes much more nuanced. Some areas are still seeing healthy price appreciation, others have leveled off, and a handful have experienced mo

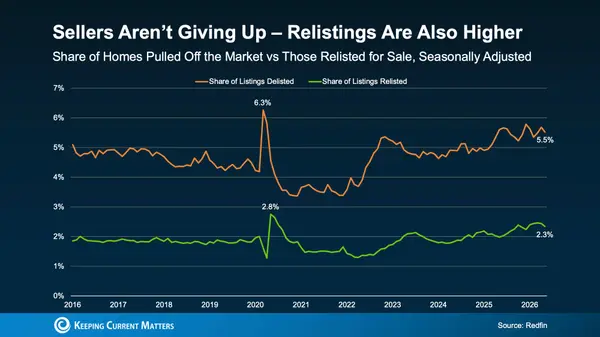

Why More Home Sellers Are Pulling Their Listings

You may have seen headlines claiming that a near-record number of homeowners are taking their homes off the market. If your first thought was, "Is this a sign the housing market is headed for trouble?" you're not alone. When more sellers decide not to sell, it can seem like they're anticipating some

Categories

Recent Posts