The Influence of the Economy on Mortgage Rates

If you're considering buying or selling a home, you're likely keeping a close eye on mortgage rates and wondering what the future holds.

One factor that can impact mortgage rates is the Federal Funds Rate, which affects the cost for banks to borrow money from one another. Although the Federal Reserve (the Fed) doesn't directly set mortgage rates, they do control the Federal Funds Rate.

The connection between these rates is why many are closely monitoring when the Fed might lower the Federal Funds Rate. When that happens, it tends to put downward pressure on mortgage rates. The Fed meets next week, and three key metrics they'll consider in their decision are:

- Inflation Rate

- Job Growth

- Unemployment Rate

Here's the latest data on each:

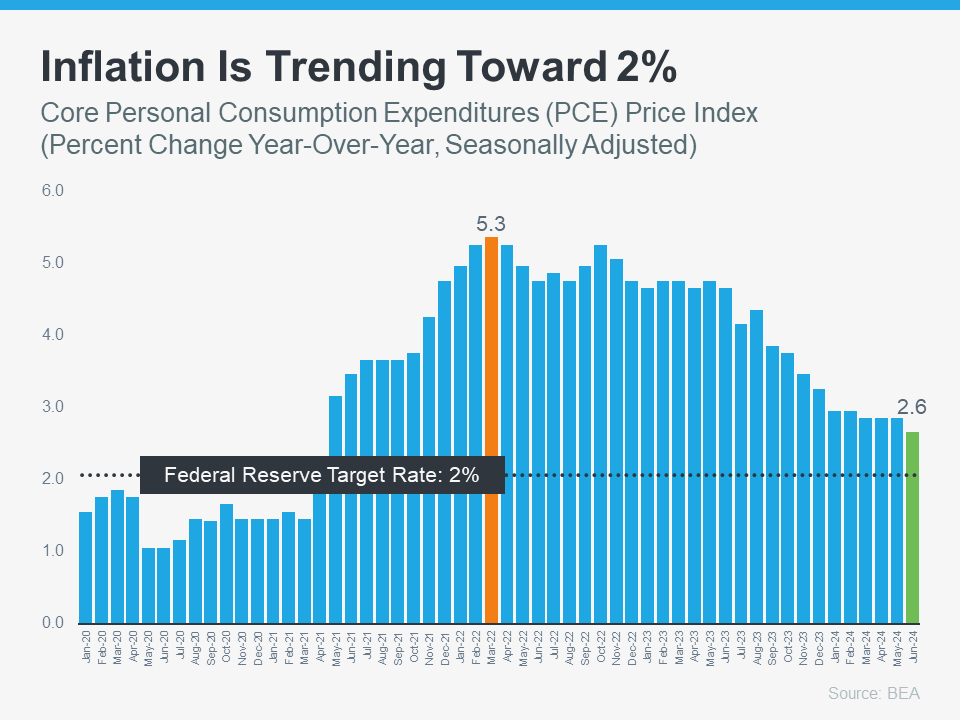

1. Inflation Rate

You've likely heard a lot about inflation over the past year or two and probably felt its impact every time you've made a purchase. High inflation means prices have been rising rapidly.

The Fed aims to bring the inflation rate back down to 2%. While it's currently above that target, it's trending in the right direction (see graph below):

2. Rate Job Growth

The Fed is also monitoring the number of new jobs created each month. They want to see consistent slowing in job growth before making any changes to the Federal Funds Rate. If job creation decreases, it indicates that the economy is still strong but cooling off slightly – which is their objective. This seems to be the current trend. According to Inman:

". . . the Bureau of Labor Statistics reported that employers added fewer jobs in April and May than initially estimated, and hiring by private companies was sluggish in June."

While employers are still creating jobs, the number is lower than before. This indicates that the economy is cooling down after a period of overheating. This trend is encouraging for the Fed.

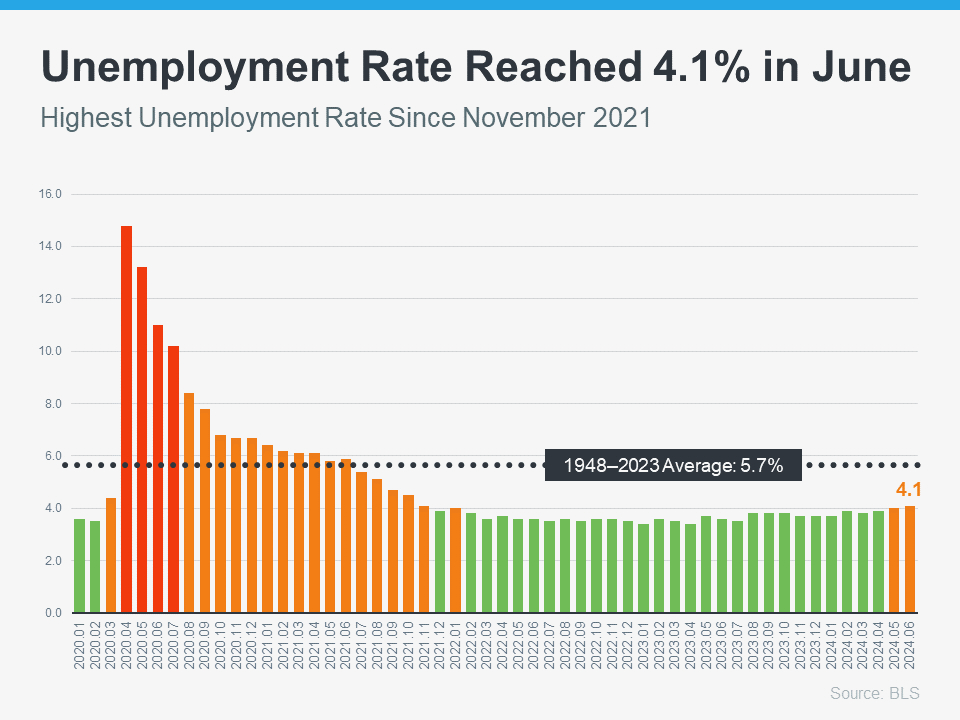

3. Unemployment Rate

The unemployment rate measures the percentage of people seeking jobs but unable to find them. A low unemployment rate indicates that many Americans are employed, which is generally positive.

However, it can also contribute to higher inflation because more employed people means more spending, which drives up prices. Currently, the unemployment rate is low, but it has been gradually increasing over the past few months (see graph below):

It might seem tough, but a steadily rising unemployment rate is something the Fed needs to observe before deciding to lower the Federal Funds Rate. A higher unemployment rate would lead to reduced spending, which would help bring inflation back under control.

What Are the Implications for the Future?

Although mortgage rates are expected to remain volatile in the coming days and months, these indicators suggest the economy is moving in the direction the Fed desires. However, despite this, it is unlikely that the Fed will lower the Federal Funds Rate at their meeting next week. Jerome Powell, Chair of the Federal Reserve, recently stated:

“We want to be more certain that inflation is consistently moving toward 2% before we begin to reduce or ease our policy.”

In essence, we're seeing initial signs, but the Fed needs more data and time to be sure this trend is consistent. If the trend continues, the CME FedWatch Tool indicates there's a projected 96.1% chance that the Fed will lower the Federal Funds Rate at their September meeting.

Keep in mind that the Fed doesn’t directly set mortgage rates. However, when they decide to lower the Federal Funds Rate, mortgage rates generally respond accordingly.

The timing of the Fed’s actions can be influenced by new economic reports, global events, and other factors, which is why trying to time the market is often not advisable.

Bottom Line

Recent economic data may suggest that there’s hope for mortgage rates on the horizon. Rely on a trusted local real estate agent to keep you informed about the latest trends and what they mean for you.

Categories

Recent Posts

GET MORE INFORMATION